*Market Poll*

JP MORGAN - Medium Term Sell

RHB - Negative/Sell

UBS - FBMKLCI 1504-1655

MORGAN STANLEY - Underweight

FIDELITY - Downward bias

NOMURA - Underweight

FX - 12 months Ringgit 4.20-4.30

ALLIANCEDBS - Buy on dips

DBS - Downside Risk

CAPITAL ECONOMICS - Sell

IHS Markit - Sell

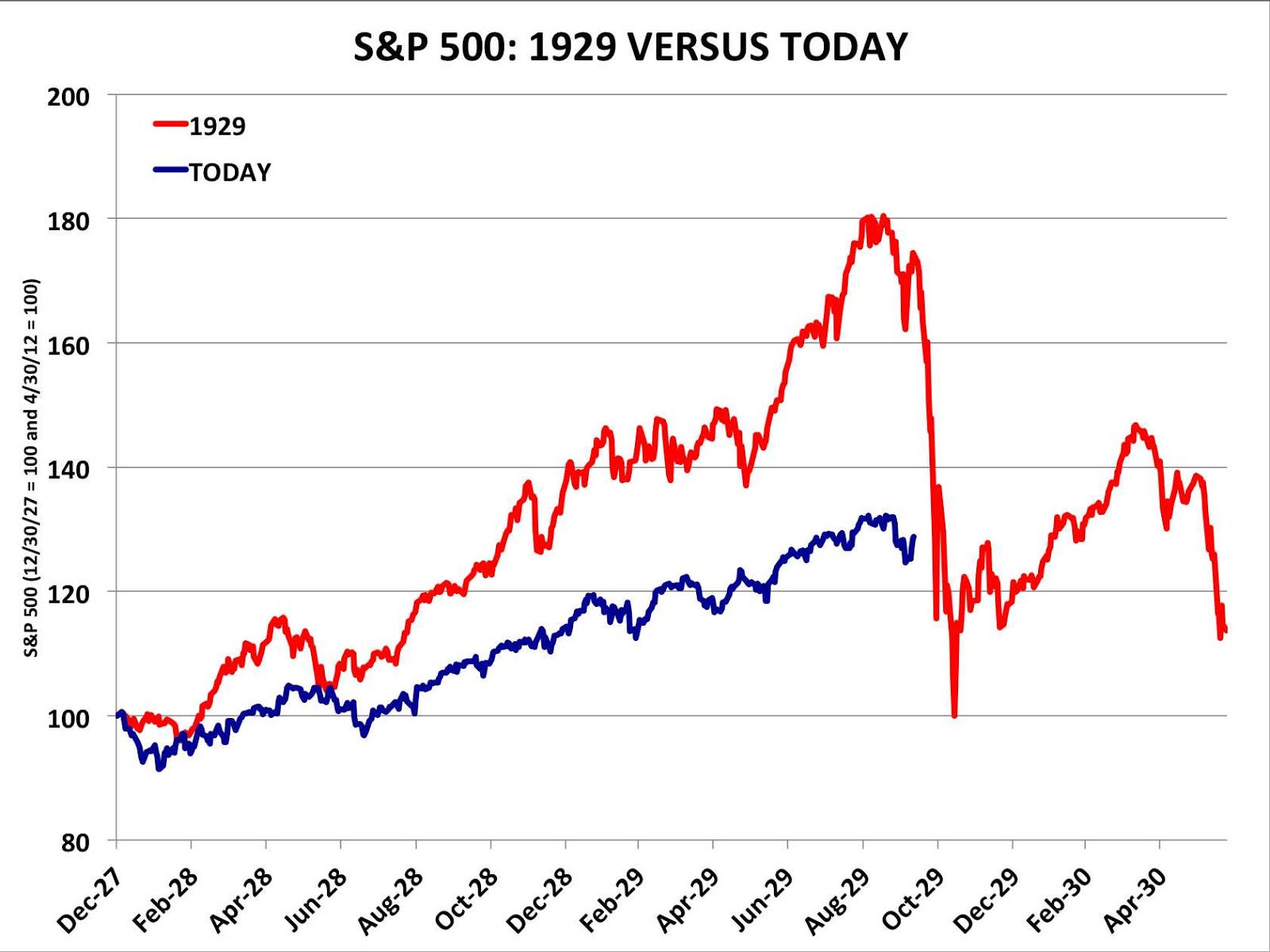

Even my favourite business magazine, covered their asses with a premature salvo. The issue arrived in my mailbox on Tuesday 8 May, the issue was dated 30 April ...

Again, we do not fathom why people get paid big bucks to write nonsense. You get the election results wrong, ok I can understand cause you may not get the pulse of the nation. Or you believed in the machinery of the previous government. Or you believed that the shennanigans, gerrymandering, scare tactics were sufficient to brush aside the power of democracy.

Not getting the election results right is one thing, not getting the reaction of the markets is less forgivable. Again, the old adage that most people get by in life by using "anchor and adjust" decision making theory. You only anchor at the previous point and adjust based on your perceptions or persuasions. There is no room for "insights" and intelligence because thats how the average get by.

So, how should we interpret the foreign net outflows:

May 14 -RM682.6m

May 15 -RM837.3m

May 16 -RM320.7m

May 17 -RM384.4m

May 18 -RM251.2m

There were naturally a lot of counters which went limit down on massive volume. There were also some counters which went limit up, but these were much fewer, and less robust compared to the selling that enveloped "limit down counters".

The KLCI went negative only briefly before restoring near parity, and even went up later.

This is my view: its not so much the net outflows, but to look at the net outflows as a percentage of actual volume traded daily. You will find that net outflows was around 10%-20% of actual volume traded. That basically told us that local institutions, and more so, retail investors, were back in taking up the slack. The net outflow figures should not be too alarming when you look at the overall picture.

False Optimism?: Would this heightened activity and positivity from local funds and retail investors be termed as "being overly optimistic"? Short answer: NO. Long answer: Definitely not! All things being equal, all the debts, excesses, mismanagement, etc... were there before and after the elections. How would a Pakatan Harapan government BE WORSE in rectifying those missteps??!!

This is my p/s view: Look at the foreign net outflow, I suspect it was not a true reflection of the mentality of foreign funds participation. I suspect a substantive amount of selling that came from "foreign funds" were some bigwigs of the past government trying to extract funds out of the country as the very platform holding up their ability to plunder in the past was shakier than a 93 year old man's walking stick (no offence to Tun).

Hence, reading between the lines, I think there is a gradual build up of genuine foreign funds coming in based on the smart/immediate steps taken by Tun M and his team.

a) Council of Elders - an immediate steadying of the ship; a brilliant move to bring back proven performers; getting Robert Kuok was a masterful move as there are a lot of substantive deals with China that needs to be renegotiated, and to pacify relations owing to some questioning of China's motives and investing strategy; an immediate strategic review and recalibration of the roles of major investing bodies...

b) Fast Action - to restore the 3 pillars of good governance, the legislative, executive and judiciary

c) Market Friendly - Tun M and Tun D, both knew how important the stock market is to the country; they have been making the right sounds and whistles

I expect certain companies will be "forced to sell" at low prices to rid of cronies of the past. It is very critical not to have a BN 2.0 infiltrating the system. Either by way of "new members joining PH for the wrong reasons" or "tainted business folks kissing new asses for survival".

Grey To Bright Gold: It will be a bit grey on the newfront initially as tallies of mismanagement, debts and hidden mistakes are brought to light. Expect a generous uptrend as assets are retrieved, savings shored up by more professional management, a more robust and transparent market for business deals, and just better management of our vast resources. Our resources just need to be managed better for the country to swiftly move back on the track of glory.