This season has not been easy for Man United, all the points were hard fought. Safe to say, this Man United team is nowhere near the quality and polish of the last team that won the Champions League, which is why its all the more satisfying. To score two goals away, Ferguson would have said well done, but after watching the match, it was a shooting gallery, Man United could have put 5 away. Somehow if we only had Ole Gunnar Solksjear, it would have been a foregone conclusion.

Still, we worry about meeting Barca in the final, which is why many would be hoping that Real Madrid can dump Barca out. However, if it was meant to be, I think meeting Barca in the final would be a good thing as Man United would be the underdog, and thats a good feeling.

Better watch the video before its banned by YouTube, its the highlights from the match.

http://www.youtube.com/watch?v=srktTCgYyBg

Wednesday, April 27, 2011

Tuesday, April 26, 2011

Japan, 1 Month Later In Pictures

A sobering yet respectful moment, the need for purpose and determination to carry on. Buddhist monks, Japan Self-Defense Force personnel, firefighters, and other relief workers observed a moment of silence on "Hiyori Yama," or Weather Hill, in Natori, Miyagi prefecture, on April 11, 2011, exactly one month after the devastating earthquake and tsunami hit northeastern Japan. Local fishermen used to climb the manmade hump and decide whether it was safe to fish. (Koichi Nakamura,Yomiuri Shimbun/Associated Press)

The picture speaks volume, at her age, did any of her family members survived, if they did not, what is she holding onto. Her thoughts must be filled with sadness and longing. An evacuee sat in a partitioned "room" at a gymnasium converted into a shelter in Kamaishi, Iwate prefecture, on April 12, 2011, a month after the March 11 earthquake and tsunami hit the northeastern coast of Japan. (Kazuhiro Nogi/AFP/Getty Images)

A good picture, its for the youth that everyone must carry on, that we should leave the world a better place for the next generation, the picture resonated hope and redemption. Rui Sato, 2, showed off his key chain while playing with a Japan Red Cross member at an evacuation center in Fukushima, northeastern Japan, on April 11, 2011. (Hiro Komae/Associated Press)

A vivid photo that emanates enormous respect for the affected families. A volunteer cleaned a family photo that was washed by the March 11 earthquake and tsunami as baby photos were placed to dry at a volunteer center in Ofunato, Iwate prefecture, April 12, 2011. (Toru Hanai/Reuters)

Shoppers looked for vegetables during a sale of produce from the city of Iwaki in Fukushima prefecture on April 12, 2011. The government is trying to support farmers in Fukushima who are hurting from dropped sales due to rumors of the spread of radiation from the troubled nuclear power plant. (Yasuyoshi Chiba/AFP/Getty Images)

Its a significant thing that there was little or no looting in the midst of the disaster, again, the photo emphasised the dignity of the human spirit - it may be swept up as trash by some, but the belongings are something of enormous value to the affected. A man looked for his personal belongings at a collection center for items found in the rubble of an area devastated by the March 11 earthquake and tsunami, in Natori, northern Japan. (Kim Kyung-Hoon/Reuters)

Events as such have been replicated in many countries, more and more, we are more connected as a planet. Greenpeace activists and other environmentalists lit candles amid hundreds of paper cranes at the Heroes' Monument at suburban Quezon city, Philippines, on April 11 in solidarity to the Japanese disaster victims. The protesters are calling for an end to nuclear power around the world. (Bullit Marquez/Associated Press)

Hope and rememberance among the ruins. A month after the tsunami devastation, 2-year-old Ayaka and family members prayed for her missing grandmother and great-grandmother at a vacant lot where they lived in Ishinomaki, Miyagi prefecture. (Yasuyoshi Chiba/AFP/Getty Images)

Monday, April 25, 2011

Was There Really A Global Recovery Since 2008?

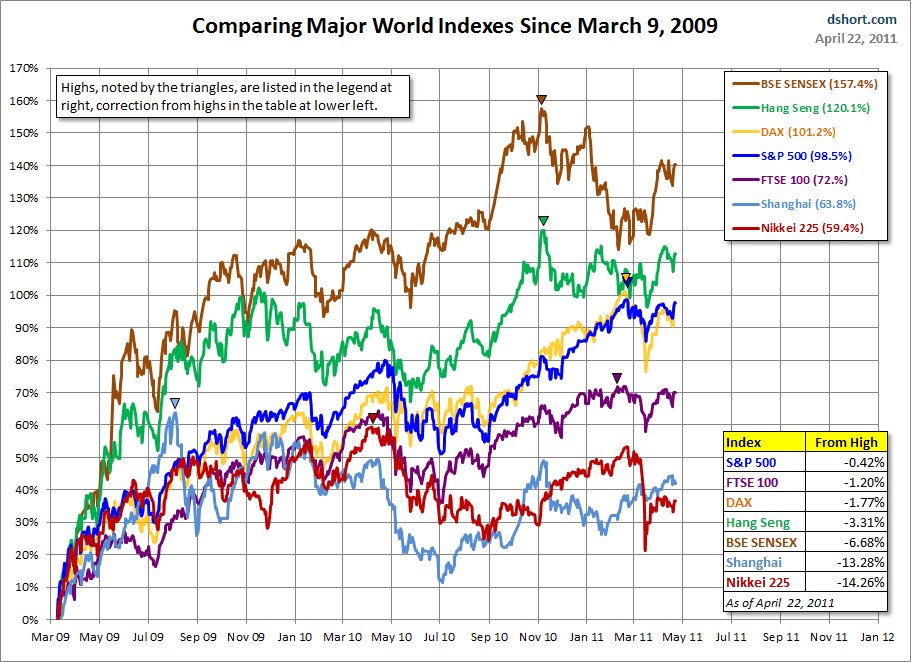

There may still plenty of naysayers about the sustainability of the global economic recovery, some might even question if there was even one in the first place. The first portion of the posting highlights the world trade and production volume. The sums have even bettered the peak right up to 2008. The second portion of the posting deals with the performance of global share markets. They have basically kept in line, although India looked terribly overbought. Hang Seng is surging next and could well have more impetus with the debasing of the USD, as more hot money will swing there to anticipate a revaluation, even without that there should be a keen chase for assets of all types there owing to the enlarging liquidity.

Despite the many major negatives, macro and external, to the global economy, much of it has been localised somewhat. The ongoing sovereign debt default issue in E.U., even the unrest in Middle East and some African nations, ... these events did rocked the markets as it should but none of the global equity markets are even ready for a correction.

Even the QE1 and 2 (quantitative easing) seems to have lent more strength to a lower USD which is not a bad thing for US stocks. Usually when you do that, interest rates will go up a lot but the recovery domestically is still muted. However, the US stock indices are not so aligned to the domestic recovery as recent weeks have show that the big boys are registering good profits growth as their tentacles are pretty much extended in emerging markets.

Following on on that, the funds have to go somewhere, owing to the growing "debasement of the USD movement" (aww shucks, you are going to hear a lot more of that new lingo), many have moved out of Treasuries. Usually in such a scenario with massive notes printed by Federal Reserve, they would go for select commodities, well gold has risen an awful lot, but thankfully gold is not a major item in the production chain. However, even though other hard commodities have rise as well, you cannot really justify the extended bullishness, in fact most hard commodities are a little over bought for now.

Oil is a unique animal, but somehow most economies have learnt to live with US$100-110 oil prices. I guess if it hits US$150 for a prolonged period, then we could see a bigger pullback in stock markets.

So, all said, funds are flowing out of Treasuries, where to? You can't all go into gold, not while corporates are registering good profit growth, which is to say, the world may have been blinded by looking too much on the negatives (all the above issues in a negative way). This is an important point, the global media, be it machinery, printed, internet or TV have tended to give a lot more airtime to blowouts, wars, QE2, oil prices, E.U. sovereign debt crisis, natural disasters ... at the expense of a more sobering look that much of the global trade and production have been chugging along nicely since 2008.

When to sell, when the Fortunes, Wall Street Journals andInternational Business Weeks start to turn bullish on stocks. Trust me, they always do that very well.

Despite the many major negatives, macro and external, to the global economy, much of it has been localised somewhat. The ongoing sovereign debt default issue in E.U., even the unrest in Middle East and some African nations, ... these events did rocked the markets as it should but none of the global equity markets are even ready for a correction.

Even the QE1 and 2 (quantitative easing) seems to have lent more strength to a lower USD which is not a bad thing for US stocks. Usually when you do that, interest rates will go up a lot but the recovery domestically is still muted. However, the US stock indices are not so aligned to the domestic recovery as recent weeks have show that the big boys are registering good profits growth as their tentacles are pretty much extended in emerging markets.

Following on on that, the funds have to go somewhere, owing to the growing "debasement of the USD movement" (aww shucks, you are going to hear a lot more of that new lingo), many have moved out of Treasuries. Usually in such a scenario with massive notes printed by Federal Reserve, they would go for select commodities, well gold has risen an awful lot, but thankfully gold is not a major item in the production chain. However, even though other hard commodities have rise as well, you cannot really justify the extended bullishness, in fact most hard commodities are a little over bought for now.

Oil is a unique animal, but somehow most economies have learnt to live with US$100-110 oil prices. I guess if it hits US$150 for a prolonged period, then we could see a bigger pullback in stock markets.

So, all said, funds are flowing out of Treasuries, where to? You can't all go into gold, not while corporates are registering good profit growth, which is to say, the world may have been blinded by looking too much on the negatives (all the above issues in a negative way). This is an important point, the global media, be it machinery, printed, internet or TV have tended to give a lot more airtime to blowouts, wars, QE2, oil prices, E.U. sovereign debt crisis, natural disasters ... at the expense of a more sobering look that much of the global trade and production have been chugging along nicely since 2008.

When to sell, when the Fortunes, Wall Street Journals andInternational Business Weeks start to turn bullish on stocks. Trust me, they always do that very well.

The CPB Netherlands Bureau for Economic Policy Analysis released its monthly on world trade and world industrial production for the month of February. Here are some of the highlights:

- World trade volume increased in February for the seventh consecutive month, bringing global trade to a new all-time record high (see chart). This was also the third month in a row that world trade was above the previous peaks during early 2008 when the U.S. recession and financial crisis started spreading, causing world trade to drop by 20% in 2009.

- World trade in February was 10.5% above its year-ago level, and marked the 14th consecutive month of double-digit annual growth starting in December of 2009. Compared to the cyclical high in April 2008, world trade volume has recovered to a level that is now 2% higher than its previous peak. Compared to the cyclical low in May 2009, global trade has increased by 28% through February of this year.

- World industrial output was the same in February compared to January, but was above its year-ago level by 7.4%. World output in the first two months of 2011 established a new, all-time record high level, which is 5.2% above the previous cyclical high of 134.4 in March 2008 (see chart above). After falling by 12% during the global recession in 2008-2009, world output has increased by almost 20% during the last two years of a strong global rebound. Global output has increased in almost every month compared to the previous month during the worldwide recovery that started in 2009, with only one month of decline in industrial output in the last two years.

Bottom Line: Based on the ongoing and solid improvements in both international trade and world output, especially the fact that global trade and production are both at all-time historical highs, I think we can now say that the world economy has made a complete recovery from the financial crisis and global slowdown in 2008 and 2009. The remarkable recovery in the global economy over the last few years is a testament to the ability of markets to recover from even a severe financial crisis and the worst economic slowdown in generations. Even though there are still many uncertainties and headwinds moving forward, the strong world economic recovery so far is both remarkable and encouraging as we hopefully have entered a new period of global growth, expansion and prosperity.

The chart below illustrates the comparative performance of World Markets since March 9, 2009. The start date is arbitrary: The S&P 500 and BSE SENSEX hit their lows on March 9th, the Nikkei 225 on March 10th, the DAX on March 6th, the FTSE on March 3rd, the Shanghai Composite on November 4, 2008, and the Hang Seng even earlier on October 27, 2008. However, by aligning on the same day and measuring the percent change, we get a better sense of the relative performance than if we align the lows.

A Longer Look Back

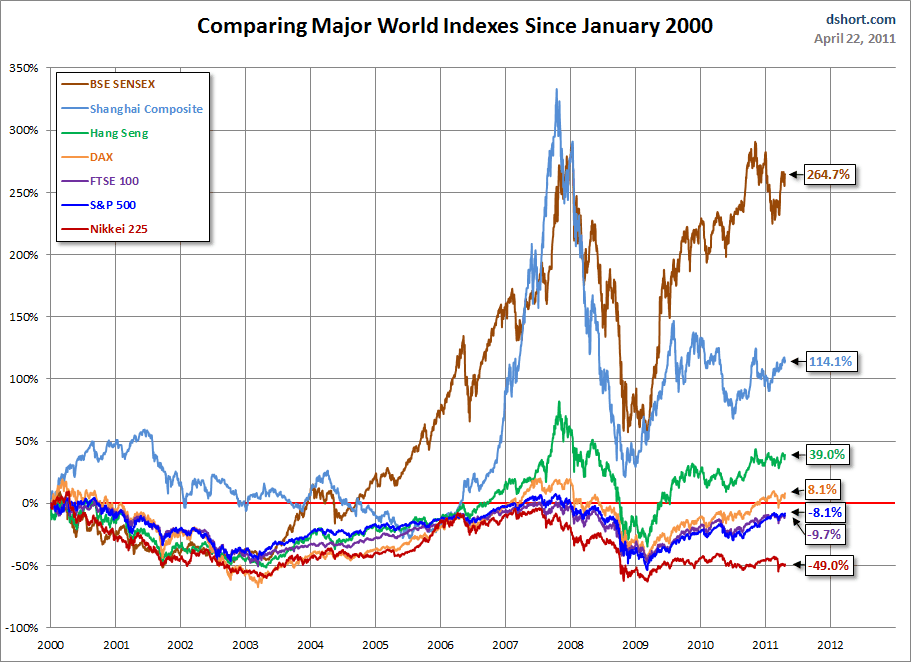

Here is the same chart starting from the turn of 21st century. The relative over-performance of the emerging markets (Shanghai, Mumbai, Hang Seng) is readily apparent. However the pattern has been less apparent over the past few months.

Tuesday, April 19, 2011

Goldman Sachs, The Sulking Boy

Power makes you do silly things. What, you did not include Goldman Sachs in your mega-IPO?? What a travesty! I will teach you all a lesson then. We are Goldman Sachs, we can make or break you, just you watch, don't you know we get a slice of all major deals globally or were you born yesterday. We can even get our government to bailout the very companies who then graciously promptly pay us back with the bailout funds.

Goldman Sachs, which ranks first in managing global share sales this year, is sulking after it didn't get an invitation to Glencore's coming-out party.

Well, do you know why Goldman Sachs was left out? I guessed its because Glencore is a huge commodities trading outfit, and Goldman Sachs is also the world's biggest trading unit in everything, including wayward human souls. I am sure they have crossed swords many times in the past, loading big, unloading big positions and is bound to ruffle each other's gilded gold feathers. You fuck me every now and then as a trading competitor, and now you want a share of my US$300m fees in my IPO, go fly your own kite Goldman.

Goldman Sachs, which ranks first in managing global share sales this year, is sulking after it didn't get an invitation to Glencore's coming-out party.

The giant Switzerland-based commodities trader is set for a dual listing in Hong Kong and London and may raise as much as US$12.1 billion (HK$94.38 billion). But Goldman is the only one of Wall Street's big investment banks not to be included in the syndicate of nine handling the float. The syndicate is expected to share in a large cake - US$300 million in fees. Goldman was left out because Glencore's board felt there was "no need" to involve it.

So, what did Goldman Sach do ... Goldman said last week that the risks of investing in commodities outweigh potential gains, dropping its recommendation to buy a basket of raw materials including crude oil, copper, cotton and platinum."Sell oil, cotton, copper, soybeans and platinum!" urged the commodities oracles at Goldman Sachs, in a surprise note last week.

Well, do you know why Goldman Sachs was left out? I guessed its because Glencore is a huge commodities trading outfit, and Goldman Sachs is also the world's biggest trading unit in everything, including wayward human souls. I am sure they have crossed swords many times in the past, loading big, unloading big positions and is bound to ruffle each other's gilded gold feathers. You fuck me every now and then as a trading competitor, and now you want a share of my US$300m fees in my IPO, go fly your own kite Goldman.

US Long Term Outlook Downgraded

U.S. stock indexes fell sharply Monday after Standard & Poor’s revised its long-term outlook on the U.S. to negative from stable. “Because the U.S. has, relative to its ‘AAA’ peers, what we consider to be very large budget deficits and rising government indebtedness and the path to addressing these is not clear to us, we have revised our outlook on the long-term rating,” the ratings agency said in a release.

My View: Well, isn't this common investing knowledge? The very same people who rated those subprime loans as AAA right up to when they collapsed, are now being seen as smart experts? I am not debating whether the ratings agencies are correct, and in this case they are. Surely this should not surprise anyone. To be fair, the US markets have to weaken in sympathy with the news even though everybody knows that to be the case.

To me, it should be seen in a positive light. China and Japan are not going to sell Treasuries, even though as an investment pro they should, but they have a lot more to lose by doing that. The ratings downgrade basically gives the US government a fixed 2 year deadline to come up with something instead of just printing and warbling some more. This will give Obama more ammunition to push through tough policy choices.

The writing was on the wall weeks ago when Bill Gross of Pimco dumped all Treasuries from its portfolio. Mind you, Pimco is the world's largest bond fund as well. Pimco has moved their assets to non-US debt, real estate and commodities.

Next was Loomis Sayles, manager of the $19.9bn bond fund, they have moved from Treasuries to high yield bonds (corporate convertibles more likely to be the case). Black Rock, another mega fund manager, has shifted to shorter term Treasuries. Even Warren Buffett has shifted his portfolio at Berkshire Hathaway, for securities maturing in less than a year from 16% of total portfolio to 23%.

What they are all doing is getting out of most Treasuries, especially the longer dated ones. This is in anticipation of a massive climb in interest rates for longer term Treasuries in the coming months and years. This implies that the US will find few takers the next few times they try to sell their long bonds to raise funds, thus forcing them to hike the interest rates for them to find takers.

That means the US dollar will be on a downtrend for the longest time and will not find takers of US denominated debts unless the interest rates are more appealing. This is also good as it forces them to come to terms with their deficits and reckless quantitative easings.

How will it affect stocks? Well, US stocks will have a kneejerk reaction but not much. The indebtedness is largely on the government side and not from the corporate side. Technically, the dollar will weaken which will be better for most US products and services.

Now, this will have a massive potential effect on the HKD peg. Its pointless to say that almost everyone is in agreement that the HKD is undervalued enormously. If the value of USD drops significantly and persistently over a long period, the HKMA may be able to brush it off. But when US rates start to rise appreciably, thus importing inflation significantly into HK's economy, something's gotta give. The longer HKMA does nothing, the more hot money will pour into HK in anticipation of an appreciation to the peg or free floating it (possibly a 10%-15% increase if they were to float the HKD now, the longer it goes on, the higher the quantum and hence the pressures).

The ratings downgrade will be good for emerging markets, well good in the shorter term (6-12 months), but bad as it will exacerbate the already excessive liquidity in many emerging markets. We should see a continued surge in US funds getting more exposure into non-US securities in the coming weeks and months.

Thankfully, the USD is not as important as it was to most Asian economies as it was maybe 10-20 years ago. More importantly for us, its the Chinese yuan. Thankfully again, most emerging markets are doing more business with each other and not just Europe or the US. Hence the macro calamities in Europe and the US would mean more funds moving to "performing emerging markets". That said, emerging markets will now have to deal more effectively with hot money and excessive liquidity running up assets of all kinds.

The rating agency effectively gave Washington a two-year deadline to enact meaningful change, just days after House Budget Committee Chairman Paul Ryan and President Barack Obama each outlined their plans for slashing debt. S&P nonetheless kept its best rating, AAA, on the U.S.

Relative to Triple-A-rated peers, the U.S. has very large budget deficits and rising government indebtedness, and the path to addressing those issues is unclear, S&P analysts said.

My View: Well, isn't this common investing knowledge? The very same people who rated those subprime loans as AAA right up to when they collapsed, are now being seen as smart experts? I am not debating whether the ratings agencies are correct, and in this case they are. Surely this should not surprise anyone. To be fair, the US markets have to weaken in sympathy with the news even though everybody knows that to be the case.

To me, it should be seen in a positive light. China and Japan are not going to sell Treasuries, even though as an investment pro they should, but they have a lot more to lose by doing that. The ratings downgrade basically gives the US government a fixed 2 year deadline to come up with something instead of just printing and warbling some more. This will give Obama more ammunition to push through tough policy choices.

The writing was on the wall weeks ago when Bill Gross of Pimco dumped all Treasuries from its portfolio. Mind you, Pimco is the world's largest bond fund as well. Pimco has moved their assets to non-US debt, real estate and commodities.

Next was Loomis Sayles, manager of the $19.9bn bond fund, they have moved from Treasuries to high yield bonds (corporate convertibles more likely to be the case). Black Rock, another mega fund manager, has shifted to shorter term Treasuries. Even Warren Buffett has shifted his portfolio at Berkshire Hathaway, for securities maturing in less than a year from 16% of total portfolio to 23%.

What they are all doing is getting out of most Treasuries, especially the longer dated ones. This is in anticipation of a massive climb in interest rates for longer term Treasuries in the coming months and years. This implies that the US will find few takers the next few times they try to sell their long bonds to raise funds, thus forcing them to hike the interest rates for them to find takers.

That means the US dollar will be on a downtrend for the longest time and will not find takers of US denominated debts unless the interest rates are more appealing. This is also good as it forces them to come to terms with their deficits and reckless quantitative easings.

How will it affect stocks? Well, US stocks will have a kneejerk reaction but not much. The indebtedness is largely on the government side and not from the corporate side. Technically, the dollar will weaken which will be better for most US products and services.

Now, this will have a massive potential effect on the HKD peg. Its pointless to say that almost everyone is in agreement that the HKD is undervalued enormously. If the value of USD drops significantly and persistently over a long period, the HKMA may be able to brush it off. But when US rates start to rise appreciably, thus importing inflation significantly into HK's economy, something's gotta give. The longer HKMA does nothing, the more hot money will pour into HK in anticipation of an appreciation to the peg or free floating it (possibly a 10%-15% increase if they were to float the HKD now, the longer it goes on, the higher the quantum and hence the pressures).

The ratings downgrade will be good for emerging markets, well good in the shorter term (6-12 months), but bad as it will exacerbate the already excessive liquidity in many emerging markets. We should see a continued surge in US funds getting more exposure into non-US securities in the coming weeks and months.

Thankfully, the USD is not as important as it was to most Asian economies as it was maybe 10-20 years ago. More importantly for us, its the Chinese yuan. Thankfully again, most emerging markets are doing more business with each other and not just Europe or the US. Hence the macro calamities in Europe and the US would mean more funds moving to "performing emerging markets". That said, emerging markets will now have to deal more effectively with hot money and excessive liquidity running up assets of all kinds.

Wednesday, April 13, 2011

For Those Who Missed The Concert

It was a wonderful concert, the video captured the excerpts from it. One thing most of the audience were not aware was that Zyan was very sick the two days leading up to Saturday. Winnie Ho (2V1G) was even roped in as a last minute replacement if Zyan's condition worsened. I have seen Zyan performed before and she did well but probably she was only 60% of herself. Lydia did magnificently well as did WVC.

Tuesday, April 12, 2011

Let's Have Some Fun

The market is in ICU, no point looking at it, let's have some fun ... discovered some gems from Britain's Got Talent, enjoy:

Jamie Pugh, quite sensational, singing my favourite song from Les Mis.

This is the unassuming Olivia Archbold, 14 year old ... they didn't allow embedding, so click on the link and be mesmerised.

http://www.youtube.com/watch?v=hWBoyoaIuAE&feature=relmfu

Now for something that will knock your socks off ... Greg Pritchard ...

and for old times sake, here a re-run on Connie Talbot .. never get tired of this, the purity of the song can only be brought out by someone so unblemished.

and after you have heard that, listen to the late Eva Cassidy (gone way too soon) rip your hearts out with her rendition .... (this live recording was done at Blues Alley 5 months before she died of cancer, so she was already very sick when she performed this)

Jamie Pugh, quite sensational, singing my favourite song from Les Mis.

This is the unassuming Olivia Archbold, 14 year old ... they didn't allow embedding, so click on the link and be mesmerised.

http://www.youtube.com/watch?v=hWBoyoaIuAE&feature=relmfu

Now for something that will knock your socks off ... Greg Pritchard ...

and for old times sake, here a re-run on Connie Talbot .. never get tired of this, the purity of the song can only be brought out by someone so unblemished.

and after you have heard that, listen to the late Eva Cassidy (gone way too soon) rip your hearts out with her rendition .... (this live recording was done at Blues Alley 5 months before she died of cancer, so she was already very sick when she performed this)

Monday, April 11, 2011

Again, Why The Ladies' Photos???

Its that time of the year to repost on why there are so many female photos on my blog. I get so many queries, I feel like this should be permanently on the sidebar. Last year, I did a Zoomerang survey with input from readers of the blog on the photos:

| How do you feel about the female photos being featured in my blog? |

| 39% | ||||||||

| 9% | ||||||||

| 31% | ||||||||

| 14% | ||||||||

| Other, please specify | 7% | ||||||||

![[2945701309_38ff8efb95_m[1].jpg]](https://blogger.googleusercontent.com/img/b/R29vZ2xl/AVvXsEhfaJsJ1yv6nDN4RBXZmQsHXjwWz74kkr_q2Vhgpud9nMfjboYLV4bLUaFe8f3s9puVkxIGGT-iTRv23yOeWjWGBV-dCSpInMLGIpn1hptS1ITse9ts-85EOXqpSqAOwye4Zt1Q/s1600/2945701309_38ff8efb95_m%5B1%5D.jpg)

I would like to add something new. Many would have noticed that I post only Asian women. Well, my blog is an "Asian blog" for starters. I also believe that the most popular lifestyle - entertainment magazines would have you believe that the most beautiful women in the world are white, blond and busty (mostly).

Surreptitiously, this is another way of reinforcing the "colonial mindset" onto the rest of the world. If you control the media, you can push for "whatever the ideal notion of physical beauty" you want. Like it or not, this plays into the kind of dolls we get for our kids. Without realising it, the cartoons, TV shows we all watch will influence our kids, and the parents as well. The whole seemingly harmless things we take for granted, the Western fairytales for example, all work to impose these kind of images and "mind censorship values system" into all who watch and listen.

I know this sounds like a desperate lawyer talking, but a healthy self-image is vital for a proper grounding to lead a happy and successful life. In no way am I bashing the Western ideals on beauty and role models, ... but we also need to be proud of our heritage and make-up. Hence all women featured are Asians only. Sigh... in my small ways, I hope to help project a healthy self-actualisation process for all (... ok, stop laughing).

I used to have to search high and low for "intelligent photos" which somehow may relate to the topic of my posting, as you can see from the first 2 years of postings. It was exhausting and not much fun at all. Postings has to have photos as its nicer to look at and more captivating. It takes me usually 15-20 minutes to write one posting, but I had to search another 20 minutes looking for a neutral photo.

Then I said to myself, its my blog, there is no need to look professional. Its all in the comments. If readers want to read it, they will read it. Why not put up photos that I liked to see. I am a very single hetrosexual guy. Hence I like pretty girls - or rather to look at them.

I don't just put up any girls, they have to be my type and have some jenaisequa' (pardon my Japanese) ... some readers prefer me not to post the photos, some really wanted me to. As for myself, I really wanted to as well. Plus they are never crude, pornographic or too revealing. If you want to just look at girl photos, there are plenty of sites for that. I also take care not to "objectify" the women, hence it is imperative that I always put up their names as well - at least it won't be like Penthouse where the girls all have just one name like Amber, Shashay, Crimson, Vandii, etc...

Lastly, its branding. There are so many business related sites. At least these are distinguishing features that sets the blog apart. I also stated that I feature only Asian ladies because this is primarily an Asian business blog. I also know of some high ranking executives who find it cumbersome to read my blog at work - they kind of have to do it secretly in case they get misunderstood... "I am really looking for the articles!!!"... but that's the fun part of it.

What I post is to share, there is no fee or subscription, or membership... in exchange I would ask my readers to "pardon my habits and indulge me a bit".

Cheers...

p/s photos: Liyana Jasmay (all photos by Photogua)

Singapore Army Jokes

Many of you would have seen the photo from Singapore which had a Singaporean soldier strolling along empty-handed, while his poor domestic helper followed carrying his military backpack.Needless to say, this was a howler of a picture, the guy was condemned left right and center. As a side note, this is one fine example of my usual rants against people who "mistreat" their maids. The same people who go shopping and then have the maid lugging tons of packages, plastic bags, etc. (way over what a normal person should) while they themselves should nothing, worse is when their children also tag along shouldering zilch. What are we teaching our children??? They are our help, not slaves. Imagine your mum or sister having to work as domestic help in an overseas country, and seeing her doing that - how do you feel, and why. Anyway, the photo brought on a whole load of jokes about the "supposedly pampered" Singapore military. Nury Vittachi put some up in his column in SCMP: http://thestandard.com.hk/news_detail.asp?we_cat=5&art_id=109980&sid=31985086&con_type=1&d_str=20110411&fc=1A NATO soldier, standing guard in the rain with a 20-kilogram pack on his back, says: "Life is hard." A People's Liberation Army soldier, standing in snow in an ill-fitting uniform, with a long march ahead, says: "Life is hard." A Singaporean army cadet, taking his iPad out of the pack his maid carried, says: "No wi- fi? WTF?" The commander sees the hopeless results of Private Tan's shooting exercises and his face falls. Tan, knowing he has done badly, says: "Sorry, sir. I feel like going to a quiet corner and shooting myself." The commander says: "Good idea, la. I suggest you take a LOT of bullets." Private Lim fails basic training and reports to the commander for punishment. The officer says: "Choose your own forfeit. One month's loss of privileges, or 20 days' pay." The Singapore cadet thinks about it. "I guess I'll take the money." As a joint exercise of Southeast Asian forces gets under way, a Malaysian general says to a Thai colonel: "I just discovered something that does the work of 50 soldiers." The Thai asks: "Really? What is it?" The Malaysian replies: "Two hundred Singaporean soldiers." The term "secure the building" means different things to different military personnel. NATO troops: "Occupy the premises and prevent anyone else entering." US Marines: "Make an all-sides armed assault on the place, and then defend it with suppressive fire." Singapore soldiers: "Take out a three-year lease with an option to buy." Seven ways the Singapore army is trying to boost recruitment: 7) Military transport flights now offer frequent-flier miles; 6) Superiors can be addressed as "Dude;" 5) Walkie- talkies replaced with latest iPhones; 4) There's always plenty of parking at the mall when you're driving a tank; 3) Radar screen toggles with user's Facebook page; 2) New uniform to be issued in Ermenegildo Zegna herringbone, with silk Hermes lining; 1) Rations now include freeze-dried Starbucks latte. The three golden rules for Singapore cadets: 1) If it doesn't move, hide behind it; 2) If it does move, surrender to it; 3) If it has four legs and isn't a table, eat it. A Singapore radio station receives a call. "This is the military. Can you tell us the exact time?" The deejay asks: "Who wants to know?" The caller says: "What difference does that make?" The deejay explains: "If you're spies, it's three o'clock. If you're pilots, it's 15:00 hours. If you're navy guys, it's six bells. If you're local army cadets, it's 120 minutes to happy hour." |

Sunday, April 10, 2011

Love This Song To Bits

What is the role of a great producer? Any one can sing a classic song of yesteryear, but once in a blue moon you get one that marry the right crossover elements in tempo, instrumentation, sensational harmonies and even new language insertions to bring forth a new way to appreciate a wonderful old song. Talk about taking mixing to the next level. Dick Lee is a masterful musician and producer (and composer). Here, with his undeniably brilliant contribution with Sandy Lam, its an exceptional song. I remember having this CD somewhere in my past life but could not locate it anymore in my collection. Luckily there is You Tube, enjoy the immaculate version of Lover's Tears!

Friday, April 08, 2011

Learn From The Japanese

While the country is still grappling to come to terms with the recent disasters, Japan still has to contend with over 1,000 of aftershocks. That is not my point, I received this email from a friend and I think we all need to ask "would we have reacted the same way in the face of a disaster or a major natural mishap". Every single country needs to ask that question, and to be honest, not many would be able to emulate how the Japanese faced adversity of the mightiest force.

Though they were open to start the "blame game" on everything and everyone, that was surprisingly mild. I know if it was in the US, a hundred and one names and institutions would have been blamed directly / indirectly for the occurence.

There was minimal panic for groceries, unlike the mad stampede in parts of China ... for salt!

Why? Why do we react differently? Is it our upbringing? We may not need to follow each and every attribute but take from each what is lacking in us, and keep asking why. Are we instilling the right values, the right priorities, the right sense of fortitude and belief through our government, as parents and as friends.

Where did the "calm" come from? How did the "suffering with dignity" aspect come about?

1. THE CALM :

Not a single visual of chest-beating or wild grief. Sorrow and introspection have been elevated.

2. THE DIGNITY :

Disciplined queues for water and groceries. Not a rough word or a crude gesture.

3. THE ABILITY :

The incredible architects, for instance. Buildings swayed but didn’t fall.

4. THE GRACE :

People bought only what they needed for the present, so everybody could get something.

5. THE ORDER :

No looting in shops. No honking and no overtaking on the roads.

6. THE SACRIFICE :

Fifty workers stayed back to pump sea water in the N-reactors. How will they ever be repaid?

7. THE TENDERNESS :

Restaurants cut prices. An unguarded ATM is left alone. The strong cared for the weak.

8. THE TRAINING :

The old and the children, everyone knew exactly what to do. And they did just that.

9. THE MEDIA :

They showed magnificent restraint in the bulletins. No silly reporters. Only calm and professional journalism minus the sensationalism.

10. THE CONSCIENCE :

When the power went off in a store, people put things back on the shelves and left quietly. That's Japan .

Though they were open to start the "blame game" on everything and everyone, that was surprisingly mild. I know if it was in the US, a hundred and one names and institutions would have been blamed directly / indirectly for the occurence.

There was minimal panic for groceries, unlike the mad stampede in parts of China ... for salt!

Why? Why do we react differently? Is it our upbringing? We may not need to follow each and every attribute but take from each what is lacking in us, and keep asking why. Are we instilling the right values, the right priorities, the right sense of fortitude and belief through our government, as parents and as friends.

Where did the "calm" come from? How did the "suffering with dignity" aspect come about?

1. THE CALM :

Not a single visual of chest-beating or wild grief. Sorrow and introspection have been elevated.

2. THE DIGNITY :

Disciplined queues for water and groceries. Not a rough word or a crude gesture.

3. THE ABILITY :

The incredible architects, for instance. Buildings swayed but didn’t fall.

4. THE GRACE :

People bought only what they needed for the present, so everybody could get something.

5. THE ORDER :

No looting in shops. No honking and no overtaking on the roads.

6. THE SACRIFICE :

Fifty workers stayed back to pump sea water in the N-reactors. How will they ever be repaid?

7. THE TENDERNESS :

Restaurants cut prices. An unguarded ATM is left alone. The strong cared for the weak.

8. THE TRAINING :

The old and the children, everyone knew exactly what to do. And they did just that.

9. THE MEDIA :

They showed magnificent restraint in the bulletins. No silly reporters. Only calm and professional journalism minus the sensationalism.

10. THE CONSCIENCE :

When the power went off in a store, people put things back on the shelves and left quietly. That's Japan .

Thursday, April 07, 2011

Got Your Tickets???

It will be a wonderful night. In addition to great songs, band and singers .. there will be video images coupled with voice overs by famous DJs to provide the right intimate setting for many of the song - it should be a romantic intimate evening for all. The evening will be centered on classic Chinese oldies and the artistes will only do very few songs from their albums. The repertoire will include those songs below (plus a few from their own albums):

夜來香 (Ye Lai Xiang : Fragrant Flower) Original Singer: Unknown

秋夜 【原唱:白光】 (Qiu Ye : Autumnal Night) Original Singer: Bai Guang

魂縈舊夢 【原唱:白光】 (Hun Ying Jiu Meng: Recurring Old Dreams) Original Singer: Bai Guang

永遠的微笑 【原唱:周璇】 (Yong Yuan De Wei Xiao: Forever Smile) Original Singer: Zhou Xuan

花樣年華 【原唱:周璇】 (Hua Yang Nian Hua: My Glorious Years) Original Singer: Zhou Xuan

忘不了的你 (Wang Bu Liao De Ni: Unforgettable You) Original Singer: Unknown

如果沒有你 【原唱:白光】 (Ru Guo Mei You Ni: If I Don't Have You) Original Singer: Bai Guang

桃李爭春 【原唱:白光】 (Tao Li Zheng Chun: Fighting For Attention) Original Singer: Bai Guang

晚風 【原唱:葉倩文】 (Wan Feng: Evening Breeze) Original Singer: Sally Yeh

恰是你的溫柔 【原唱:蔡琴】 (Qia Shi Ni De Wen Rou: Like Your Tenderness) Original Singer: Cai Qin

不了情+新不了情 【原唱:萬芳】 (Bu Liao Qing + Xin Bu Liao Qing: Endless Love (new and old) Original singer: Unknown/Wan Fang

秋詩篇篇 【原唱:劉家昌】 (Qiu Shi Pian Pian: Autumnal Poetry) Original Singer: Liu Jia Chang

我只在乎你 【原唱:鄧麗君】 (Wo Zhi Zai Hu Ni : I Only Care For You) Original Singer: Teresa Teng

往事只能回味 【原唱:尤雅】 (Wang Shi Zhi Neng Hui Wei: The Past Can Only Be Reminisced) Original Singer: Yu Ya

red denote RM105 seats. blue denotes RM85 seats

red denote RM105 seats. blue denotes RM85 seats

夜來香 (Ye Lai Xiang : Fragrant Flower) Original Singer: Unknown

秋夜 【原唱:白光】 (Qiu Ye : Autumnal Night) Original Singer: Bai Guang

魂縈舊夢 【原唱:白光】 (Hun Ying Jiu Meng: Recurring Old Dreams) Original Singer: Bai Guang

永遠的微笑 【原唱:周璇】 (Yong Yuan De Wei Xiao: Forever Smile) Original Singer: Zhou Xuan

花樣年華 【原唱:周璇】 (Hua Yang Nian Hua: My Glorious Years) Original Singer: Zhou Xuan

忘不了的你 (Wang Bu Liao De Ni: Unforgettable You) Original Singer: Unknown

如果沒有你 【原唱:白光】 (Ru Guo Mei You Ni: If I Don't Have You) Original Singer: Bai Guang

Untitled from Leslie Loh on Vimeo.

桃李爭春 【原唱:白光】 (Tao Li Zheng Chun: Fighting For Attention) Original Singer: Bai Guang

晚風 【原唱:葉倩文】 (Wan Feng: Evening Breeze) Original Singer: Sally Yeh

恰是你的溫柔 【原唱:蔡琴】 (Qia Shi Ni De Wen Rou: Like Your Tenderness) Original Singer: Cai Qin

不了情+新不了情 【原唱:萬芳】 (Bu Liao Qing + Xin Bu Liao Qing: Endless Love (new and old) Original singer: Unknown/Wan Fang

秋詩篇篇 【原唱:劉家昌】 (Qiu Shi Pian Pian: Autumnal Poetry) Original Singer: Liu Jia Chang

我只在乎你 【原唱:鄧麗君】 (Wo Zhi Zai Hu Ni : I Only Care For You) Original Singer: Teresa Teng

往事只能回味 【原唱:尤雅】 (Wang Shi Zhi Neng Hui Wei: The Past Can Only Be Reminisced) Original Singer: Yu Ya

red denote RM105 seats. blue denotes RM85 seats

red denote RM105 seats. blue denotes RM85 seatsTicketing Info:

Concert Date: 9th April 2011 (Saturday)

Time: 8.00pm

Venue: Bentley Auditorium, Mutiara Damansara

Price: RM105 & RM85 (See Seating Plan. Seat allocation will be done at auditorium entrace, first come first serve basis.)

Ticketing Outlets:

CDRAMA (Popular Bookstore) Ikano Power Centre (03-77258188/5832)

CDRAMA, Sunway Pyramid (03-56377280/7286)

CDRAMA, Cheras Leisure Mall (03-91322435/437)

Loud+Clear, Solaris Dutamas (03-62111683)

Concert Date: 9th April 2011 (Saturday)

Time: 8.00pm

Venue: Bentley Auditorium, Mutiara Damansara

Price: RM105 & RM85 (See Seating Plan. Seat allocation will be done at auditorium entrace, first come first serve basis.)

Ticketing Outlets:

CDRAMA (Popular Bookstore) Ikano Power Centre (03-77258188/5832)

CDRAMA, Sunway Pyramid (03-56377280/7286)

CDRAMA, Cheras Leisure Mall (03-91322435/437)

Loud+Clear, Solaris Dutamas (03-62111683)

Tuesday, April 05, 2011

Marketocracy Portfolio As At 5th April 2011

| |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| |||||||

| |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| |||||||||||

| |||||||||||

| |||||||||||||

| |||||||||||||

| |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Close Date | Type | Symbol | Shares | Net Avg. Price | Net |

|---|---|---|---|---|---|

| Mar 23, 2011 | Buy | PVSW | 8,977 | $6.1055 | $54,809.44 |

| Mar 22, 2011 | Buy | PVSW | 1,018 | $5.8247 | $5,929.55 |

| Mar 21, 2011 | Buy | PVSW | 7,224 | $5.6197 | $40,596.67 |

| Mar 21, 2011 | Buy | CIM | 25,000 | $4.3091 | $107,727.33 |

| Mar 21, 2011 | Sell | BP | 3,000 | $45.563 | $136,688.89 |

| Jan 14, 2011 | Buy | NSR | 2,500 | $27.0218 | $67,554.43 |

Subscribe to:

Posts (Atom)

may i know why there is beautiful girl picture posted when you talking landmark and statistic?

10:14 PM