The PEG ratio is the P/E ratio over the growth rate, and a PEG of less than one is generally considered good, according to Bespoke - however, guys, that is almost none existent. For example if a country is looking at GDP growth of 20%, can we safely try to find the markets at just 20x PER. Generally if you can even get a figure of 3, that is very decent already.That is we are talking of GDP growth rates and not company earnings growth rates. Even the very robust China markets only showed 10%-12% GDP growth in their robust years, so the 1/1 things never will exist.

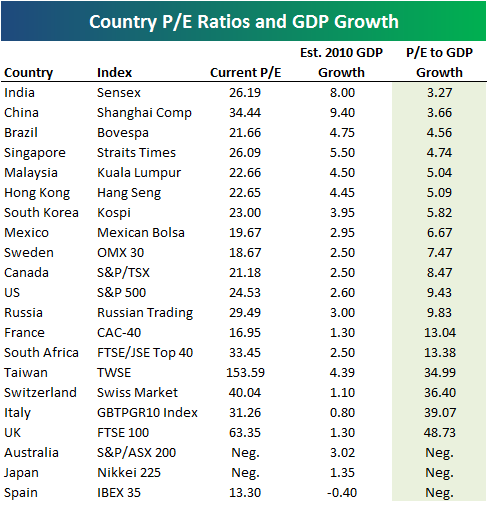

In this regard, they have created "PEG" ratios for a number of countries using the P/E ratio of each country's main equity market index along with 2010 estimated GDP growth rates. Just as with stocks, the lower the country PEG, the more attractive.

click to enlarge

Worries over political stability should be ebbing now that Najib seems to have stood the "uncertain first year" in the office. Many funds were adopting a wait and see attitude with respect to Malaysia as many were thinking that many issues and factors were very "volatile" and fluctuating in the first few months. I think that stage has passed.

Bank Negara has managed very well, not letting the economy dwindle and keeping a lid on pessimism. The catalyst for Malaysia will be the ringgit outlook. I do think Bank Negara will be allowing the ringgit more leeway going forward, and that is a major attraction to funds. Valuation wise, its not demanding. The domestic economy is flushed with liquidity, just go to any new property launches. These are all a potent mix.

p/s photos: Jarah Mariano

1 comment:

The PERs look like they are based on 2009 earnings as most regional PERs are below 20x for 2010.

If they are using 2010 GDP growth rates, they should use the same year for PER.

Post a Comment