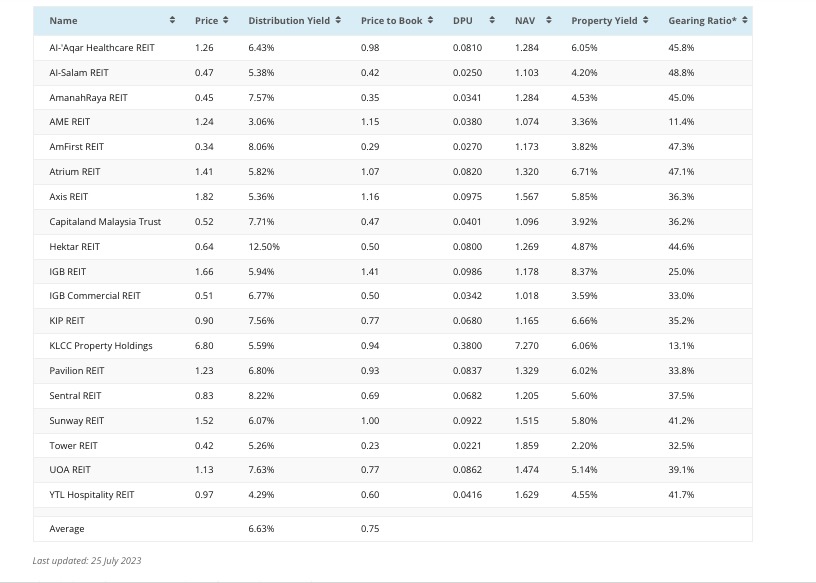

A friend asked me about Malaysian REITs... they all look so cheap. What gives. Looking at the above table there are only 5 REITS that trades at its NAV or higher: AME, Atrium, Axis, IGB, and Sunway.

If you look at Price to Book, i.e. discount to NAV, many trade between 40%-70% discount to NAV. How should we view such investments?

Discount Trap/Value Trap

Most REITs do trade at a discount, that's a given, but an acceptable discount should only be between 5%-15%, anything more implies there's something more that we have missed out.

Potential Factors Driving Discounts:

a) an environment of higher interest rates, which eats into net yield as rentals are not so agile at moving in tandem with real interest rates... not to mention the higher cost of refinancing;

b) economic activity outlook depressing: if we are looking at a depression over the horizon, there will be more breaking of leases and rentals, and subsequent downward pressure on yields;

c) owing to the age/design of properties under management, investors may be looking at lower rentals going forward, thus exacerbating the discount;

d) diversification or non-diversification can and will affect the discount, and so too is the "Grading" of the said property;

e) vacancy rates, the existence of newer competing projects in surrounding areas, the deterioration of infra-supporting business activity;

f) the aging aspect and requirements for repairs and upgrades;

g) the liquidity being traded, as usual, a bigger REIT would always win over a smaller capitalized REIT, the ability to get in and out, the ability to get a sizable position;

h) more importantly: access to more capital sources, transparency, and a good management team;

Locally, investors are most gloomy with Hotels and Resorts type REITs. Will take a few more years before we need to look at them. Investors are most keen on Healthcare related REITs. The other sub-sector that is slightly optimistic is the Office REITs, while the Industrial REITs are not that exciting, although nowhere as gloomy as Hotels/Resorts REITs.

Using Discounts Smartly

REITs Rosetta Stone

Local REITs taxation (or rather the non-taxation aspect) is the key. If the government even starts to consider any policy change to tax them, it will be more than disastrous. However, if we follow the regional policy to stay competitive, that is not likely to happen anytime soon.

What Do I Prefer

Well, good management first of all. I also like to look at family-owned REITs. There are family-owned ones that have good and solid professional management and some that don't. Do they do arm-length transactions?

The other aspect I look at is how "dependent" they are on the yearly dividends. To that end, I mean that the shares and other equity instruments are "not sold" or held in trust, and the rest of the family relies on the dividends more so than others.

I prefer UOA, IGB and KIP. But that's just me.

No comments:

Post a Comment