We think a property worth RM600,000 in 2007 is now worth RM1.8m. We cite rising land cost, material costs, labour cost, easy loans, blah blah ...its all a reflection of overwhelming liquidity prompted by low interest rates. but how can easing in the US by the Fed, BOJ or ECB affect us in Malaysia. The reality is that it does and very easily so... low rates promotes carry trades, and search for higher yields = emerging and developing markets' assets (currency, property and stocks).

The same house could very well go back to RM1.0m in a global soaking up of liquidity. Of course the naysayers will remind us that these central banks will be ever slow to buy back bonds (soak liquidity). If these central banks won't do it, the markets will do it for them. When will we correct, when most people are bulls. The many bull runs from 2009 till today in various markets have been "not welcomed" because not "enough investors" have jumped back in yet. Much of the liquidity is still sidelined.

So when? I think another massive global property run up may just do the trick. So we may be 1-2 years away at least.

--------------------------------------------------------------

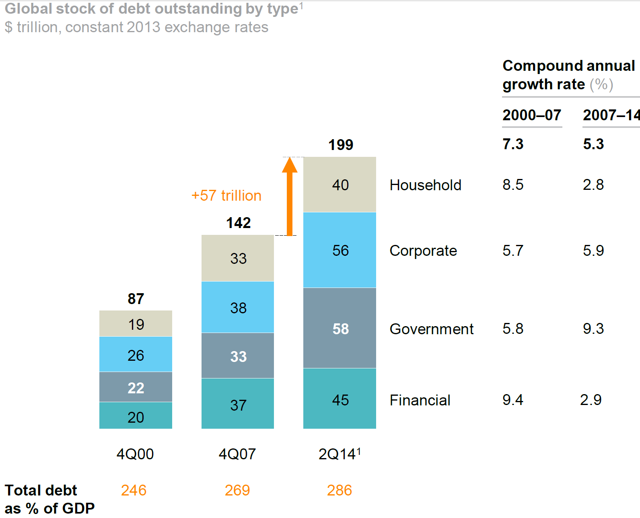

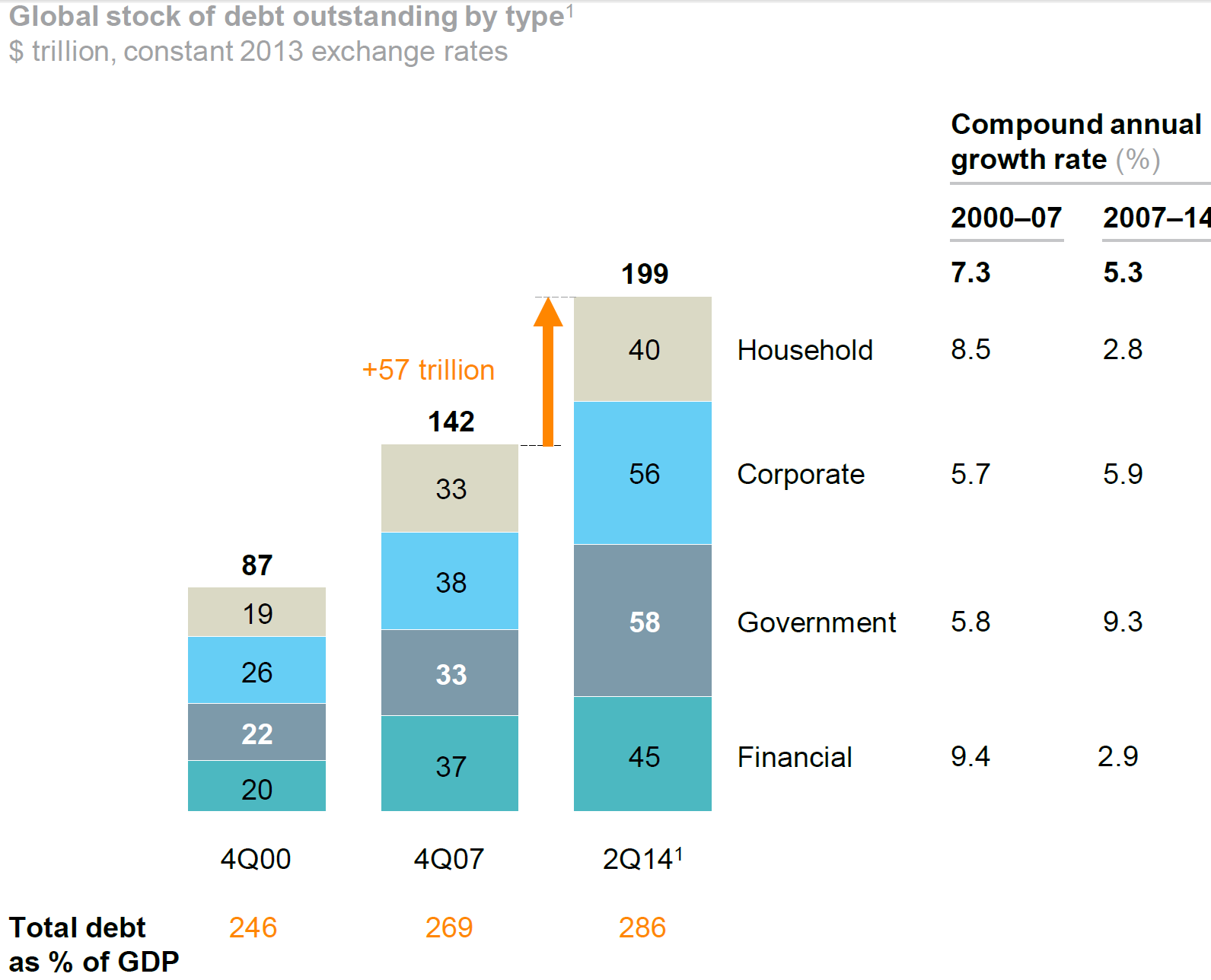

There is a stunning chart that all gold investors need to see and understand that was recently released by McKinsey Global Institute - it covers the latest update on the worldwide debt situation.

(click to enlarge)

Source: McKinsey Global Institute

There are two main things that investors should take away here. First, the world is not deleveraging as global debt loads have grown $57 trillion over the last seven years to $199 trillion - that is a huge amount of debt. To put that into perspective, the total market capitalization of the whole S&P 500 is around $20 trillion; so every two and half years the world is taking on the equivalent of every single S&P 500 company in NEW debt!

Taking on new debt by itself isn't necessarily unsustainable if productivity and growth are increasing at a faster rate than the debt load. That is where we come to the second point - debt is growing faster than worldwide GDP.

We have never been a fan of GDP as a hard number because it is a very political number and cannot be reliably calculated, but even if we put this aside and use government estimated GDP numbers, the data above shows debt as a percentage of GDP is getting larger. According to the McKinsey calculations, global debt rose from 269% of worldwide GDP to 286% over the last seven years, which in layman's terms means that the world has increased its debt faster than its production.

This is simply not sustainable as no economy can grow its debt faster than its productivity - something has to give.

What Happens Next

With debt growing at a faster rate than GDP, eventually the money won't be there to service the debt load and default will ensue. The fear that we have wouldn't be related to a single default, but rather, it would be related to the collapse in confidence that would occur in the debt markets.

As the table above shows, the growth in debt despite all-time low interest rates means that investors are very confident in ability of the indebted to pay back their debts OR in the ability of investors to sell these debts to others (i.e. the greater fool theory). That must be the case otherwise we wouldn't be seeing growing debt levels while interest rates are falling around the world.

Also, investors tend to forget that growing government debt levels artificially raise productivity. Economist David Stockman explains it best:

The implied 2.9X global leverage ratio is daunting in itself. But now would be an excellent time to recall the lessons of Greece because the true implications are far more ominous.Today's raging crisis in Greece was hidden from view for many years in the run-up to its first EU bailout in 2010 because the denominator of its reported leverage ratio-national income or GDP-was artificially inflated by the debt fueled boom underway in its economy.In other words, it was caught in a feedback loop. The more it borrowed to finance government deficit spending and business investment, whether profitable or not, the more its Keynesian macro metrics-that is, GDP accounts based on spending, not real wealth-registered a falsely rising level of prosperity and capacity to carry its ballooning debt.

Investors that think they can escape a debt crisis by purchasing stocks with low debt levels may find their whole investment thesis completely obliterated. These "safe" companies will find that their revenues will also tumble as they were the second and third order beneficiaries of expanding debt spending.

The world has been spending beyond its means, as evidenced by growing debt loads as a percentage of GDP, and when that confidence in the debt ends, not only will interest rates rise but global growth will plummet as many projects will no longer be funded by belt-tightening debtors. This will only accelerate investor worries about their debt holdings - a vicious cycle.

What Does This Have To Do With Gold?

Now, we come to gold. It should be obvious now that globally we are massively over-leveraged with debts which are not sustainable as debt growth now dwarfs economic growth despite record-low interest rates. When this reality sets in with investors, we will start to see money leave debt instruments and move to assets that are unrelated or negatively correlated to debt - the ultimate one being "cash."

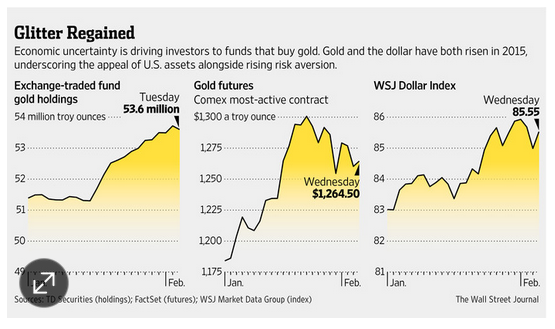

We may already be seeing this as the traditionally negative relationship between gold and the US Dollar has evaporated over the past few months.

Source: The Wall Street Journal

We think the US Dollar is not as safe as investors believe (and certainly not as safe as gold), but this is a discussion for another day. The take-away here is that the recent strong positive correlation between gold and the US Dollar may be the result of investors starting to question the increasing global debt load.

Investors will seek assets that can perform well when there is panic or even defaults in the debt market - gold is clearly one of the few assets historically that has done very well when debts have performed poorly.

Conclusion for Gold Investors

Contrary to what some analysts have been suggesting, the world has not been deleveraging since the financial crisis, and in fact has been growing its debt loads. Not only is total debt growing, it is growing at a faster pace than global growth, and it is doing so despite the strong tailwind of all-time low interest rates. Everything about this is not sustainable and at some point we will start to see defaults - which will cause panic in debt markets and interest rates to rise.

Thus wise investors will be seeking investments that do well when debt instruments do poorly, and that will lead them to gold. So while investors and fast-money traders in the gold market are focusing on frivolous short-term things like the recent US jobs report and the latest omission from the Fed minutes, they are clearly missing the forest for the trees as unsustainable global debt loads are a ticking time bomb.

Finally, we think the real opportunities will be in the gold explorers, as their valuations are much lower than the miners and the fact of the matter is that these gold miners will be looking to expand reserves and buying out the quality explorers, so we'd suggest investors be aggressively investing in these quality explorers. For those interested in explorers or investors interested in keeping up with the gold market on a consistent basis consider following us (clicking the "Follow" button next to my name) or join our free email list where we send out a weekly email summarizing all the important events in the gold and silver industry, including all of our latest articles and research - it's a great way to keep up with the gold and precious metals market whether you are an individual investor or economist and its completely free.

Now is the time that investors should be buying assets that are uncorrelated to the debt markets - gold is the asset that has historically performed well when we have debt market panics. Investors shouldn't miss the forest for the trees here and get caught up in short-term price moves - there is a debt-crisis brewing and investors better be prepared with some gold investments.

3 comments:

Yay. The babes are back

my question is not if we should keep some gold. My question is, how do you valuation the gold price? Since it's hardly a traditional commodity to actually use in our daily life, it's extremely difficult to put a value to it. Warran Buffett said it's overvalued, so do many others. What do you think?

Hi Dali,

I'm new to gold/silver investment.

I need some advise. For example, Maybank gold/silver investment it seem did not back by any physical gold/silver. Is maybank help investor to purchase US ETF? In this scenario what is the greater risk?

If US debt is too high will it cause USD devaluation, and what is the impact?

Kindly advise.

Thanks

Post a Comment