The local stocks have been in the doldrums for the longest time. We are talking of at least 4-5 years with the exception of a big run on glove stocks during the pandemic. The market is huge and it takes a lot of factors to collide for it to mushroom into a full-blooded bull market.

Malaysia has one of the highest GDP/market capitalization of stock exchange companies in the WORLD. Please wrap that around your finger. We are talking of 80 odd percent of local GDP. Every time a company starts to make RM4-6m a year, investment bankers will start shadowing those companies and groom them for a listing. The only companies not listed in Malaysia are your laundromats, kedai runcits, cendol seller, etc...

PM Anwar and his team have inherited a poor economy with loads of issues. At the same time, we are battered by the flight of money away from local shores owing to the presence of a new government. Plenty of "gray wealth" has left the shores thus exacerbating the ringgit's strength.

PM Anwar and Rafizi know too well how they need to supercharge the economy while taking time to curtail past misdeeds on our balance sheet. PM announced that Forest City has been designated as a special financial zone to spur the economy in Iskandar Malaysia. Amongst the incentives that have been announced include multiple entry visas, fast-track entry for those working in Singapore, and a flat income tax rate of 15% for knowledge workers. He said this should spur the growth of those involved in the healthcare, education, and tourism sectors.

Now, that announcement was in the middle of August... have a look at UEMS chart:

(UEMS 30 sen to 70 sen rally is about +130%; as the leader and th one with the biggest landbank the rally is still early)

Our superboy has been picking up steam since the middle of July from 30 sen, and it's around 70 sen in less than 1.5 months. OK forget about the fact that someone, somewhere... will also hear about the news first. Where do we go from here? Can this be big and sustainable enough to spark a broader bull run? Or will it just fizzle out?

My Views

a) The announcement by the government is not a haphazard thing; it is a thought-out plan with eventualities mapped out on logistics, people movement issues, visa issues, the proper monitoring and regulatory side on Forest City, etc.

b) This is certainly big enough to trigger a broader market rally; the concept... remember Putrajaya in 1995... that was a concept ... in 2001 it is real, viable, and operating; the same here, Forest City is not a concept, while it has not been fully built out yet, there are sufficient developed parcels to jump-start the whole new concept.

c) Political will: The Federal is for it, they need something big to revive the economy and hope to stand a better chance of winning the next general elections; We all know the Johor state government has been waiting for a long time to kickstart this mega project; and Singapore is exactly at the property cycle whereby, it needs to move the industrial sites to cheaper locales, to the Singapore side, this is the best alternative for them but they CANNOT be seen as the one proposing the scheme as that might be construed as a "takeover or buyout"; this way its more accommodating, you scratch my back I scratch yours.

The Johor Bahru-Singapore Rapid Transit System (RTS) is not a new project. It started in 2020 and will only be completed in 2026. While MyHSR Corporation recently initiated a request for information (RFI) to solicit concept proposals from local and international players for the behemoth Kuala Lumpur-Singapore high-speed rail project, the bankability of any public infrastructure project of this scale is always in question, however, with this new development, the "success factor" for this will be bettered substantially.

d) As explained earlier, our local economy is intrinsically tied to our stock market; what it means is that it has a very high BETA, i.e. you pump RM100m into the stocks, it will have a velocity of money of around 7x-9x to the real economy; making it imperative to jumpstart the local economy; thus the Federal will move mountains to ensure that this gets delivered and executed promptly and smartly.

(IOI Prop's rally from 1.10 to 1.60 is about a 45% gain; that's a lagging performance and should have the legs to test RM2.00 soon)

The above table is a useful guide but I would also consider real float /controlling shareholders' real interest/ funding capacity/ stale bulls on the way up.

What's Next

Now, we need subsequent REAL CATALYSTS, and they need to come every few weeks. The newsflow will have to be positive and consistent.

Catalyst #1: This one has to happen soon. Since PM Anwar's announcement, I have been scouring the pages of The Straits Times to read any news or opinions from the government down south. The silence was deafening. Seriously, nothing of substance, just the announcement, nothing from the related ministries or PM down south. This just makes it more LIKE and PALPABLE that some major announcement will come soon. That's because obviously, it looks like a huge collective PR and rhetoric will come soon to applaud how the plan will enhance every facet of Singapore's economy and future prosperity.

Catalyst #2: There has to be REAL DEMAND, the real movement of companies. That should come from MNCs and some Singapore GLCs to start with, followed by local Singapore companies. Once timelines is heard and seen, these catalysts will further enhance the rally in stocks.

Catalyst #3: To restart many of the projects, they will need funds. Foreign companies coming to JV will be big catalysts as well. Fundraising will take center stage, thus providing more climaxes for the local bourse.

Catalyst #4: Asian stocks have been a blur over the past few years. The Forest City is a sufficiently big enough idea to draw back foreign investors. Keep an eye on the level of foreign buyers in local stocks over the coming months.

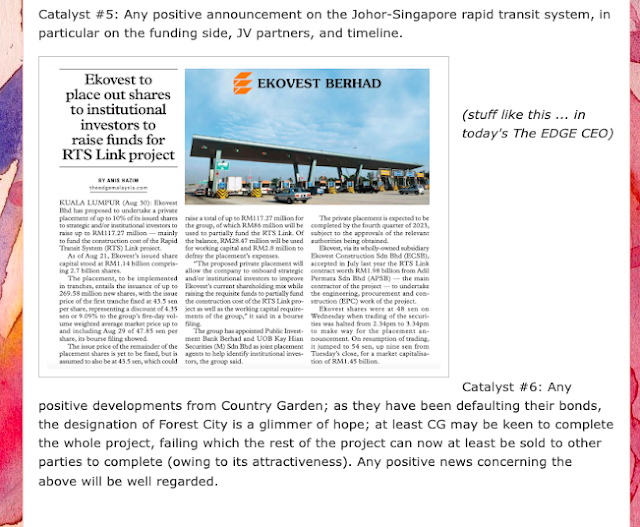

Catalyst #5: Any positive announcement on the Johor-Singapore rapid transit system, in particular on the funding side, JV partners, and timeline.

(stuff like this ... in today's The EDGE CEO)

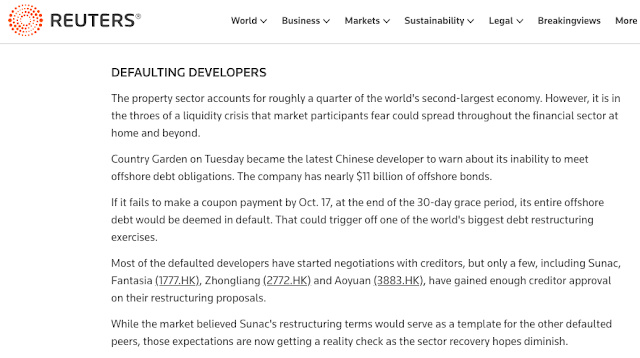

Catalyst #6: Any positive developments from Country Garden; as they have been defaulting their bonds, the designation of Forest City is a glimmer of hope; at least CG may be keen to complete the whole project, failing which the rest of the project can now at least be sold to other parties to complete (owing to its attractiveness). Any positive news concerning the above will be well regarded.

Final View: Yes, I think this has a solid chance to propel a big rally in local stocks.

Let's look at the LINKED stocks:

(Sunway's run from 1.60 to 1.90 is only a gain of 18%, judging from the factors above 2.50 should not be difficult)

(Somebody forgot to inform them, that it ran up only 9% from 1.40 to 1.52; looks to have some legs yet)

(by virtue of them being a small taikor in Johor; access to mid-priced projects; delivering very solid profits; and having substantial landbank in and around Johor; this has lots of legs; just the run from 85 sen to 1.11, a 30% gain is insufficient to account for just the spectacular profits, and we are not even talking of their Johor exposure)

(up 53% from 60 sen to 92 sen; think there are better counters to ride the coattails)

Disclaimer: This is not a call to buy or sell, just an opinion from a market watcher, please consult your dealer or remisier before any action.