Growing distrust in the central banks

During the last round of the global financial crisis, bold decisions made by central banks around the world did avert a collapse of the then fragile economic systems. The loose monetary policies adopted in the US have probably rescued the nation from entering into another "Big Depression" as we knew in the 1930s. Nonetheless, the zero interest rate policy (ZIRP) has been in place for more than a "considerable period". The economy has not been able to grow in a robust manner as in the previous economic rebounds. The average annual GDP growth is around 2.5% in the aftermath of the 2008 crisis. Chairperson of the Fed, Dr. Janet Yellen, said once the economy is strong enough to stand on its feet, the Fed would start increasing the Federal fund rates gradually and "with patience." With the revised GDP growth in Q314 standing at 5% and the unemployment rate at 5.5% last December, many stock investors probably believe our economy is indeed the best among the G-7 countries. They expect the Fed start hiking rates later this year. The bond investors, nevertheless, beg to differ.

Look at the price actions of the US long-term government bonds in the past 12 months. iShares Barclays 20+ Years Treasuries Bond Fund (NYSE:

TLT) is a very popular ETF betting on the appreciation of the fund price when interest rates go down. What the chart is revealing is that bond investors do not believe that the Fed would honor its words. Put it in a more diplomatic manner, they do not believe the Fed would not be able to raise rates because there is very little economic growth both in sight and in the pipeline. The latest statement from one of the Fed's top officials did contain such ambiguity. Last Friday San Francisco Federal Reserve Bank President John Williams said:

"There is no need to rush to raise rates; at the same time we want to make sure that we appropriately act in a way that we don't get behind the curve. If the forecast evolves the way I expect, six months from now or whatever - middle of this year - I think we'll have a better position to understand either well we need to wait longer, or maybe it's we could act now."

(click to enlarge)

Source: Stockcharts.com

The chart simply shows that the bond investors who are always considered to be more prudent, if not more intelligent, have ruled out any chance of a rate hike in 2015. If they had listened to the talk of the Fed and trusted what the Fed would do, the prices of the Treasuries would have been gone down instead of going up. When it comes to bond investing, high interest rates would always bring bond prices down and vice versa.

There are good reasons not to trust the central banks. The sudden reversal of the Swiss National Bank (SNB) last week to de-peg its national currency from the Euro is the best example to show how a central bank could dishonor its commitment overnight. Few days before the policy reversal, the central bank vowed that the peg was a "cornerstone of the country's monetary policy." Nonetheless, the good intentions of SNC to prevent global funds from flowing into Switzerland during the Euro zone crisis resulted in a fast accumulation of foreign currency reserve. In order to cap the exchange rate of one Euro to 1.2 franc, SNB ought to keep the printing press rolling to enable it to keep buying Euro. This is the only alternative in a current peg to keep the Swiss franc from going strong. However, the declining Euro due to anemic economic growth in the Euro zone has proved to be a financial burden too much for the country.

(click to enlarge)

Source: Swiss National Bank

The de-pegging decision led to an immediate 10% plus rise in the value of Swiss franc against almost all major currencies. Many retail and institutional investors were caught unprepared. The "Black Swan" has created havoc in the financial markets. The sudden unexpected upswing in the Swiss franc has caused bankruptcy of two relative small foreign currency traders in the UK and New Zealand - Alpari and Global Brokers NZ.

In the US, a New York-based currency broker FXCM, confirmed late Friday that it was getting a $300 million rescue loan from financial firm Leucadia National Corp. The online currency trader was about to breach regulatory capital requirements following a $225 million loss by its clients overnight.

(click to enlarge)

Source: Stockcharts.com

Trading resumed in the after-hours on Friday and the last trade was at $4.3. Compared with the stock's closing price at $17 one week prior, the stock lost 75% of its value. The extent of financial instability brought about by an unanticipated move of a major central bank cannot be underestimated.

The global currency trading market is huge estimated at nearly $2 trillion turnover per day on the spot market. The real carnage to major US banks and other financial institutions are unknown as of now. Regulators in New Zealand, Hong Kong, Britain and the United States said they were checking on brokers and banks to assess the consequences after reports of volatility and losses. The incident shows that any change of mind by any major central bank on set policy goals would send ripples or cause severe turmoil to the global financial system.

The incident serves to remind stock investors that they should not place complete trust in decisions of the central banks. Take the Bank of Japan (BOJ) for example. The unprecedented stimulus program launched by BOJ in the past two years has failed so far to bring the country out of deflation. The 2% inflation rate it vowed to reach remains a remote target. On the contrary, the trade surplus Japan used to enjoy for decades because of its stellar export performance has turned negative. The current account is in the red. The national debt keeps rising to over two times of its GDP. Many critics suggest that the failure of BOJ's QE program would lead the country and even the world into uncharted waters.

A critic on Reuters Breakingviews who is skeptical about the ability of central banks to fight deflation reminded investors that central bankers are not omnipotent. Here is what the columnist

Swaha Pattanaik wrote:

"Swiss monetary policy did not work as planned. The Bank of Japan, and the ECB, which is expected to launch a government bond-buying program soon, may not be any more successful. The U.S. Federal Reserve and the Bank of England do not have to worry much about stimulating growth now, but if they do, their arsenals are depleted"

The ECB chief Mario Draghi vowed to do "whatever it takes" to save the Euro in 2012. He succeeded. On Thursday, when the ECB announces its scheduled plan to resurrect the Euro zone inflation, I believe the market would not respond mildly to the long overdue solution. Any disappointment might lead to another round of havoc or volatility in the financial markets. Against this kind of uncertainty, retail investors must monitor the equity markets closely or take profits first to protect their portfolio.

Gold is again becoming a sought-after safe haven

Like the Swiss franc and the greenback, gold has always been a safe haven when fears abound. In the past three years, investors dumped gold because the precious metal failed to serve as a hedge against inflation. Nor could it generate any recurrent income for the yield-hungry investors. The everlasting function of gold as a safe haven has never vanished. The recent turnaround of gold against the ever-stronger US dollar implies that a pocket of investors is finding the macro-environment worrisome. They are re-examining the value of the long-neglected asset class as a "currency" besides its universally accepted status as a safe haven during bad times.

Some investors have already moved in. According to Bloomberg, holdings in the SPDR Gold Trust (NYSEARCA:

GLD), the biggest exchange-traded product backed by the metal, surged the most in more than four years. Assets in the SPDR fund jumped 1.9 percent to 730.89 metric tons last Friday when the metal closed at $1,280 - a four-month high. The holdings climbed 3.3 percent last week. With regards gold futures, call options for the right to own February futures at $1,300 an ounce soared sevenfold in two days

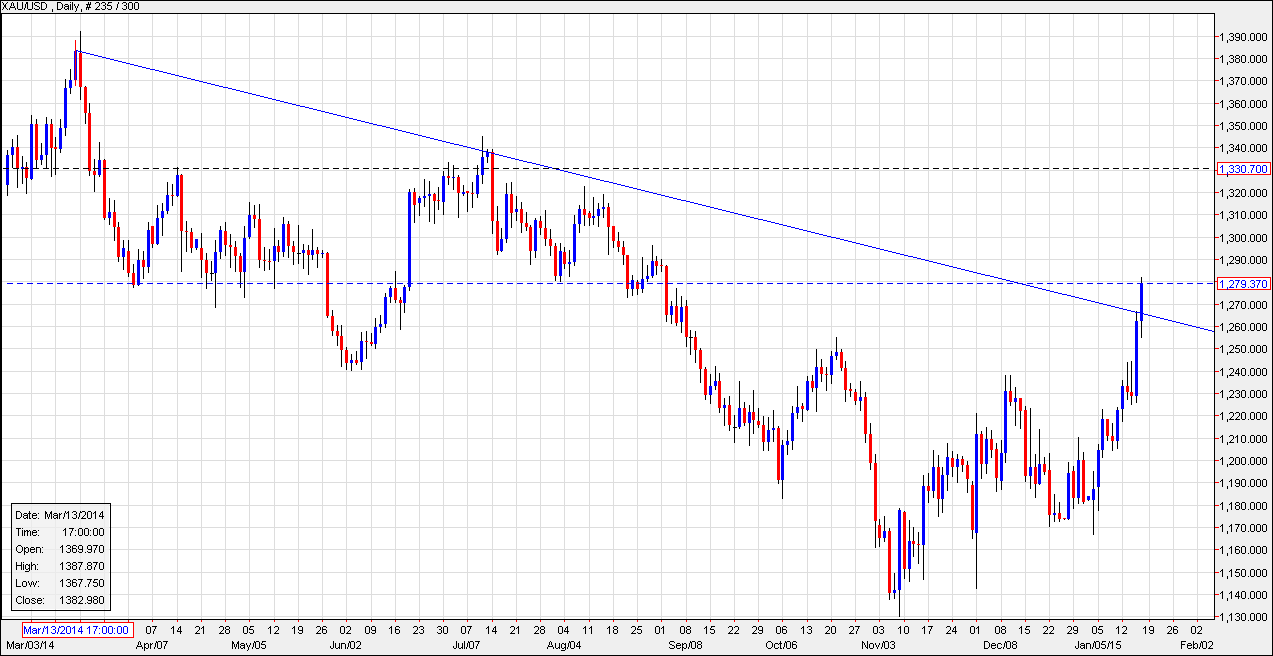

As of last Friday, gold has increased 12% from the 52-week low recorded last November. Most importantly, gold has two important technical breakthroughs. First, it broke above the downward daily trend line extended since last March.

(click to enlarge)

Source: Stockcharts.com

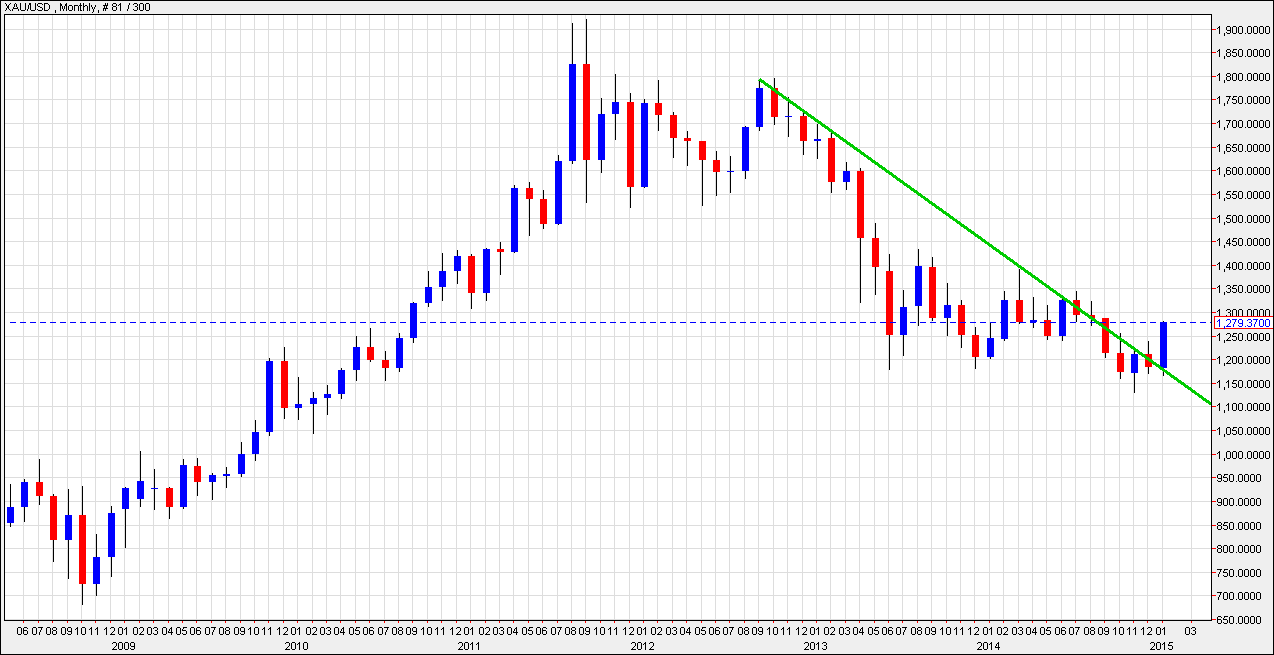

Second, in the monthly chart below, the gain in January 2015 represents a conspicuous breach above the down trend line extended from late 2012. This could be a very meaningful technical breakthrough, hinting that the time for a long-term turnaround is coming provided gold could retain its current strength by the end of the month.

(click to enlarge)

Source: Stockcharts.com

The fact gold regains the favor of investors is not by coincidence. The growing mistrust in the central banks may have led to a trend reversal of the gold prices. The concerns about an upcoming deflationary environment i.e. the first red flag mentioned at the beginning of this article are probably another contributing factor.

"It is living up to its reputation as a safe haven as other cyclical commodities are tumbling, equity markets are down, and we are seeing higher risk aversion almost everywhere."

"Gold is popping because fear is coming back into the marketplace and gold is regaining its stature as a safe-haven commodity. Look at what has happened with the global central banks today. The surprise - you know - black-swan move by the Swiss National Bank is not creating more confidence; it is creating less confidence. And people are running back to gold."

Author of the well-known investment letter Gloom Boom Doom Report, Marc Faber also attributed the growing fear to the failure of central banks to deliver what they promise. He expected gold could jump 30% in 2015.

"My belief is that the big surprise this year is that investor confidence in central banks collapses. And when that happens - I can't short central banks, although I'd really like to, and the only way to short them is to go long gold, silver and platinum."