Thursday, June 28, 2012

Friday, June 22, 2012

Wednesday, June 20, 2012

This Will Be A Great Concert

When Liu Chia Chiang meets Li Zhong Shen. I was not brought up on Mandarin popular music, if anything, I am more a Canto-pop kind of guy. However, if you examine the musical landscape of Mandarin music, no greater giants can you find other than the two names mentioned, from the 70s right up to the 90s. Naturally I prefer Li Zhong Shen, his lyrics already kills me most of the time and the melodies are superb as well.

Leslie Loh the producer has this to say when I asked him to elaborate why this concert is unmissable:

1) this is winnie ho's latest concert, and her only major concert in 2012, fresh from her sensational solo album! like her or not, you can't deny she can sing and very well at that!

2) it has two fantastic guest male singers in ah worm and ah fei

3) it has tay cher siang yet again. who doesn't know TAY CHER SIANG by now?

4) we are singing songs from the two most respected and legendary composers in the chinese pop history: jonathan lee and liu jia chang. together these two godfathers are responsible for evergreen classics too many to count!

5) winnie ho and tay cher siang are malaysia's treasures and they will carry the malaysian flag proudly abroad in the very near future. be the early supporters rather than late supporters cos it is cooler that way!

6) be part of the FIRST CHINESE JAZZ MOVEMENT in malaysia!

7) it is held in bentley music auditorium again, the 2nd best hall in malaysia after DFP in terms of acoustics

8) ticket price are only RM125 and RM85, well worth the price for a full-scale jazz production

9) you get to meet hundred of like-minded chinese jazz lovers under one roof! and lastly,

10) the organizer is pop pop music, you can't expect anything less from us (ahem, blowing a big trumpet!)

Indulge me while I share this song Ling Wu, so heartbreaking, to know and understand, to realise after just how great and wonderful they were together. Both LZS and Sandy Lam were married to each before, I cannot help but feel they were singing about each other. Beautifully aching, to say the least, ... who showed more regret and emotion?

The other LZS song that mesmerises me, the melody and lyrics ... OMG...

Leslie Loh the producer has this to say when I asked him to elaborate why this concert is unmissable:

1) this is winnie ho's latest concert, and her only major concert in 2012, fresh from her sensational solo album! like her or not, you can't deny she can sing and very well at that!

2) it has two fantastic guest male singers in ah worm and ah fei

3) it has tay cher siang yet again. who doesn't know TAY CHER SIANG by now?

4) we are singing songs from the two most respected and legendary composers in the chinese pop history: jonathan lee and liu jia chang. together these two godfathers are responsible for evergreen classics too many to count!

5) winnie ho and tay cher siang are malaysia's treasures and they will carry the malaysian flag proudly abroad in the very near future. be the early supporters rather than late supporters cos it is cooler that way!

6) be part of the FIRST CHINESE JAZZ MOVEMENT in malaysia!

7) it is held in bentley music auditorium again, the 2nd best hall in malaysia after DFP in terms of acoustics

8) ticket price are only RM125 and RM85, well worth the price for a full-scale jazz production

9) you get to meet hundred of like-minded chinese jazz lovers under one roof! and lastly,

10) the organizer is pop pop music, you can't expect anything less from us (ahem, blowing a big trumpet!)

buy your tickets at Popular CD-RAMA at ikano power center (IPC) or telephone booking at 012-2083790

Indulge me while I share this song Ling Wu, so heartbreaking, to know and understand, to realise after just how great and wonderful they were together. Both LZS and Sandy Lam were married to each before, I cannot help but feel they were singing about each other. Beautifully aching, to say the least, ... who showed more regret and emotion?

The other LZS song that mesmerises me, the melody and lyrics ... OMG...

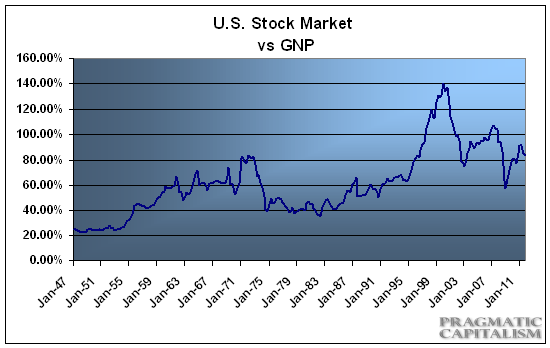

Buffett's Most Realiable Indicator ... Not For Us

Buffett has said before that the total market cap vs. GNP is one of his preferred valuation metrics. The current reading of 89% is still above his preferred buying range (70-80%), but well off the highs we've seen in the last 15 years. Buffett has previously explained his thinking behind the indicator:

Yes, its a good indicator, but a very basic indicator akin to above or below NTA. If you are buying below 100%, you are "safer", its not rocket science. This indicator ranges from 60%-140% of GNP owing to the US economic structure.

One has to bear in mind that the market cap vs GNP relationship is very different for other countries.

One of my favoured economist, Chua Hak Bin, wrote on the same topic some time back, with an Asian flavour:

Malaysian Economy More Sensitive to Crashes

The Malaysian economy is however more sensitive to crashes. The representation of households who own shares directly or indirectly is probably similar to the U.S. profile. The market capitalisation of the KLSE is however about 320 percent of GNP. This implies that a 30 percent crash in the KLSE amounts to the equivalent wipe-out of 96 percent of GNP. If the stock of wealth is about 10 times GNP, this still amounts to a dissappearance of about 10 percent of total wealth. Such a sharp fall in wealth will inevitably hurt consumer spending.

The Malaysian economy's sensitivity to stockmarket crashes has been increasing over time with the rising market capitalisation of the KLSE. During the 1987 crash, Malaysia's stockmarket capitalisation accounted for only about 90 percent of GNP. As such, the ripple effects from the 1987 crash did not have such far reaching consequences. However, with the capitalisation accounting for more than 300 percent, Wall Street's sentiment may have become inevitably linked to the Malaysian economy. This worrisome conclusion extends to Hong Kong and Singapore whose market capitalisation have both exceeded 250 percent as well.

TABLE: THE MALAYSIAN ECONOMY IS OVEREXPOSED TO A STOCKMARKET CRASH

Some Comforting Thoughts

There are some important factors to account for when linking market capitalisation to total wealth. First, the rather high market capitalisation of the Kuala Lumpur, Singapore and Hong Kong stockmarkets are partly a result of its openness to foreign investors. As such, a large fraction of the market capitalisation is "foreign wealth" rather than "domestic wealth." The fraction will be higher in Singapore and Hong Kong than Malaysia. If the fraction of Malaysian shares which are foreign-held account for as much as 30 percent, then the true "domestic market-capitalisation to GNP" that matters for calculating the local "wealth effect" is reduced to only 224 percent.

Second, consumption is dependent on permanent rather than current wealth. Consumers take into account their future income when deciding on their habits today. If the fall in the stockmarket is regarded as temporary rather than permanent, consumers will not treat the loss as a real loss but a temporary paper loss. As a result, consumers will not reduce their spending as sharply when faced with the fall in current wealth. A word of caution is noted however as empirical studies have provided evidence that consumption is linked to current rather than permanent wealth due to the existence of credit constraints.

My Comments: It is not the Asian markets openness that causes the 300% market cap vs GNP, or anything to do with foreign investments. Rather, its the listing mentality of the respective countries coupled with the "designed rules". In Malaysia, once you start making RM3m-5m a year, there will be predators coming to you thinking of ways to list your company.

This makes for a much lower threshold to list companies in Asia (generally) than elsewhere. Hence you may generalise that the only things not listed in Malaysia are the mamaks and mechanics (though some of the bigger mamak chains make quite decent bucket loads of money, but then they have to worry about paying real taxes if they were to list them properly).

Of course we can still use the market cap vs GNP indicator for the Malaysian market alone, maybe the range over a 20 year period could be between 200% to 400%, and you surmise that anything below 300% might be a "safer" buying territory. To me, its still more b.s. than anything.

Hence we can also surmise that a market correction of 25% in the US and a similar 25% correction in Malaysian, Singaporean and HK markets are very different. The latter 3 countries will see a more pronounced real money flow effects (shrinkage and reduced velocity of money). In most of Europe the normal indicator is around 50%, which is to say a market correction has less real impact on the real economy as a large portion of the economy there are still not listed.

That indicator is shallow and does not relate or take into account the dynamics of the markets. For example, you can tally up the holdings of indexed stocks in Malaysia held by local funds, esp local government or GLC funds. Without the exact data, I can say it has been a substantial rise over the past 10 years, in particular over the last 5 years.

What that means may be that the index could be easier to "control". This will also mean that you may be able to "engineer better" a stock market sell down, or the reverse as well. Just think how well you could "control the index" if you hold 25% of all indexed stocks, what if its 35% or 45%, maybe 65% later on.

The amount of local funds have been mushrooming and EPF has really no space to put it anymore, which is why they have to think of overseas. The other local funds have also been growing as well. Its all good and well if it does not get to the level whereby there is more "manipulative streaks" than a genuine "investing strategy for better returns". The bigger danger is that if you hold a strong hand, you could also close a stock price "artificially higher every year end" to maintain the appearance of good performance for your overall funds, even though in reality the fundamental performance of the said stock may be not exciting.

The powers to be has to be fully aware of the potential distortion this may bring and prevent this scenario from ever occurring. We are not there yet, but we need to be on guard owing to rise in investible funds in our country.

"For me, the message of that chart is this: If the percentage relationship falls to the 70% or 80% area, buying stocks is likely to work very well for you. If the ratio approaches 200%-as it did in 1999 and a part of 2000- you are playing with fire."

So stocks aren't cheap, but they're also not terribly expensive based on this measure. If the recent trend holds we could be nearing Buffett's preferred buying range in the coming years….

(click to enlarge)

Yes, its a good indicator, but a very basic indicator akin to above or below NTA. If you are buying below 100%, you are "safer", its not rocket science. This indicator ranges from 60%-140% of GNP owing to the US economic structure.

One has to bear in mind that the market cap vs GNP relationship is very different for other countries.

One of my favoured economist, Chua Hak Bin, wrote on the same topic some time back, with an Asian flavour:

Malaysian Economy More Sensitive to Crashes

The Malaysian economy is however more sensitive to crashes. The representation of households who own shares directly or indirectly is probably similar to the U.S. profile. The market capitalisation of the KLSE is however about 320 percent of GNP. This implies that a 30 percent crash in the KLSE amounts to the equivalent wipe-out of 96 percent of GNP. If the stock of wealth is about 10 times GNP, this still amounts to a dissappearance of about 10 percent of total wealth. Such a sharp fall in wealth will inevitably hurt consumer spending.

The Malaysian economy's sensitivity to stockmarket crashes has been increasing over time with the rising market capitalisation of the KLSE. During the 1987 crash, Malaysia's stockmarket capitalisation accounted for only about 90 percent of GNP. As such, the ripple effects from the 1987 crash did not have such far reaching consequences. However, with the capitalisation accounting for more than 300 percent, Wall Street's sentiment may have become inevitably linked to the Malaysian economy. This worrisome conclusion extends to Hong Kong and Singapore whose market capitalisation have both exceeded 250 percent as well.

TABLE: THE MALAYSIAN ECONOMY IS OVEREXPOSED TO A STOCKMARKET CRASH

| Countries | Market Cap/ GNP (%) | Fall in Value from 30% Crash as Percent of GNP |

| Malaysia | 320 | 96 |

| Hong Kong | 290 | 87 |

| Singapore | 250 | 75 |

| Bangkok | 109 | 33 |

| London | 105 | 30 |

| New York | 70 | 21 |

| Bombay | 38 | 11 |

| Jakarta | 35 | 10 |

Some Comforting Thoughts

There are some important factors to account for when linking market capitalisation to total wealth. First, the rather high market capitalisation of the Kuala Lumpur, Singapore and Hong Kong stockmarkets are partly a result of its openness to foreign investors. As such, a large fraction of the market capitalisation is "foreign wealth" rather than "domestic wealth." The fraction will be higher in Singapore and Hong Kong than Malaysia. If the fraction of Malaysian shares which are foreign-held account for as much as 30 percent, then the true "domestic market-capitalisation to GNP" that matters for calculating the local "wealth effect" is reduced to only 224 percent.

Second, consumption is dependent on permanent rather than current wealth. Consumers take into account their future income when deciding on their habits today. If the fall in the stockmarket is regarded as temporary rather than permanent, consumers will not treat the loss as a real loss but a temporary paper loss. As a result, consumers will not reduce their spending as sharply when faced with the fall in current wealth. A word of caution is noted however as empirical studies have provided evidence that consumption is linked to current rather than permanent wealth due to the existence of credit constraints.

My Comments: It is not the Asian markets openness that causes the 300% market cap vs GNP, or anything to do with foreign investments. Rather, its the listing mentality of the respective countries coupled with the "designed rules". In Malaysia, once you start making RM3m-5m a year, there will be predators coming to you thinking of ways to list your company.

This makes for a much lower threshold to list companies in Asia (generally) than elsewhere. Hence you may generalise that the only things not listed in Malaysia are the mamaks and mechanics (though some of the bigger mamak chains make quite decent bucket loads of money, but then they have to worry about paying real taxes if they were to list them properly).

Of course we can still use the market cap vs GNP indicator for the Malaysian market alone, maybe the range over a 20 year period could be between 200% to 400%, and you surmise that anything below 300% might be a "safer" buying territory. To me, its still more b.s. than anything.

Hence we can also surmise that a market correction of 25% in the US and a similar 25% correction in Malaysian, Singaporean and HK markets are very different. The latter 3 countries will see a more pronounced real money flow effects (shrinkage and reduced velocity of money). In most of Europe the normal indicator is around 50%, which is to say a market correction has less real impact on the real economy as a large portion of the economy there are still not listed.

That indicator is shallow and does not relate or take into account the dynamics of the markets. For example, you can tally up the holdings of indexed stocks in Malaysia held by local funds, esp local government or GLC funds. Without the exact data, I can say it has been a substantial rise over the past 10 years, in particular over the last 5 years.

What that means may be that the index could be easier to "control". This will also mean that you may be able to "engineer better" a stock market sell down, or the reverse as well. Just think how well you could "control the index" if you hold 25% of all indexed stocks, what if its 35% or 45%, maybe 65% later on.

The amount of local funds have been mushrooming and EPF has really no space to put it anymore, which is why they have to think of overseas. The other local funds have also been growing as well. Its all good and well if it does not get to the level whereby there is more "manipulative streaks" than a genuine "investing strategy for better returns". The bigger danger is that if you hold a strong hand, you could also close a stock price "artificially higher every year end" to maintain the appearance of good performance for your overall funds, even though in reality the fundamental performance of the said stock may be not exciting.

The powers to be has to be fully aware of the potential distortion this may bring and prevent this scenario from ever occurring. We are not there yet, but we need to be on guard owing to rise in investible funds in our country.

Monday, June 18, 2012

Sunday, June 17, 2012

Peut-etre Le Best Breadmaker In The Country ....

Pardon my attempt at basic French, went for a nice and easy Saturday morning hunt for the bread maker that has been given rave reviews by some of my friends. So it is with guarded expectations and muted anticipation that me and my special friend went searching for this little gem. We were not disappointed.

Its a tiny place but from what I know, they already have established a solid reputation and is supplying excellent breads to many restaurants and luxury hotels. We tried two of their four most popular breads for sandwiches, very good to excellent. A warning, their portions are generous to a tee.

The story goes that Tommy went backpacking to France but stayed on for years to learn how to make bread, so romantic, passionate ... how not to fall in love with his products.

http://tommylebaker.blogspot.com/

To get a full sense of Tommy's vision, passion and motivation, let him speak for himself:

"My passion for baking and the desire to revive the traditional values of craftsmanship in bread-making are the qualities that drive the essential spirit behind “Tommy Le Baker”.

My offerings are carefully made to restore bread-making to the highest standards of the craft. And more importantly, to recapture the original flavours sought by masters of the tradition.

Kneaded, shaped and baked on-site: the specially selected ingredients, time-tested methods, and unmistakable oven-baked freshness of Tommy Le Baker make every slice, loaf or piece of pastry truly a rare indulgence.

Modern means of production, managed with heartfelt care for the final outcome on a fussy selection of flours, grains, seeds, butters and oils allow me and my artisans to offer you the best kinds of fresh bread likely to be found anywhere in Kuala Lumpur.

In addition, where ever possible, I have been absolutely faithful to traditional recipes, while looking to support our local merchandisers and produce.

In the culmination of my time-tested methods, the finest ingredients, and a desire to produce only the best you may find in my bakery-café traditional favourites from artisanal viennoisseries, pâtisseries, gateaux de voyage, to even long-forgotten French regional specialities.

Come sit for a while here in my little bakery, surrounded by a plethora of the baker’s paraphernalia and instruments of his craft, and imbibe the sights, smells and tastes of the art of baking.

Here, you may enjoy fine coffees, popular soft drinks, and the occasional soup servings to accompany breads and pastries fresh out of Tommy Le Baker’s ovens.

Through my modest bakery, I hope you will join with me in my passion for good things, especially our breads: a significant part of culinary history that has brought joy, nutrition and life to mankind since time immemorial."

The lemon tart, which was raved by many, to me was good but not mind blowingly so. Still its a pretty good tart, 8/10. Should try. We tried their house cake, the La Joncha, or the Mona Lisa, it is simply possibly the best cake both of us have ever tasted. Its layered, it may not look like much but its divine. Each of the layers presented different textures to the whole cake and yet somehow each contributed exquisitely to the whole experience. There is the soft cream, the ice cream smooth moose, the delectable rich chocolate holding the whole cake together ... its just a wonderful cake experience. I am not exaggerating if I say this is 10/10 for a cake.

Love the guy, he is affable, personable, genuine, and you can feel his passion emanating through what he does. Love his mum too. Nice touch at the end, a personal hand written receipt, it kind of signs off on a lovely lazy afternoon, ... I am a happy boy!

Tommy Le Baker: Specializes in pre-ferments and long fermentation process to nurture the taste and to achieve the full nutritional potential of bread using what the nature has provided to his baker.

Address

B-0-7 Viva Residency,

378, Jalan Ipoh

(Opposite KLPAC)

Tel (03) 40432546

Opening hours

Tues - Fri, 10am - 8pm

Saturday, Sunday, Public Holiday , 10am - 6pm

Close on Monday

Friday, June 15, 2012

Wednesday, June 13, 2012

Colour Me Blue

There is black and white

but we know no one can be completely unblemished or the other extreme

Knowingly or unknowingly, we take on shades of grey

Some start from white while some tries to lighten from the dark side

Politics and business, you cannot have one without the other

We all can be different shades of grey

but there is a difference when you knowingly keep adding black to the mix

We all can be shades of grey

but there is a difference when we keep trying to move towards white

The really sad part about my country is when grey is the colour of choice

and I see no outcry when there is injustice and unfairness

Grey silences us all

Grey locks up our integrity and do not allow our true values to come to the fore

Grey shuns difficult paths

and takes the safest and easiest path to myob

When your grey keeps taking on black

you start to forget about the sanctity of white

The balance of powers reside too close to the power magnet of black

Is this how a society loses its soul

Colour me blue

Monday, June 11, 2012

What Is Your Investing Values' System

Like it or not, we all practice some sort of value system when we buy and sell shares, knowingly or otherwise. If you have no value system, then you are among a small group of people, your mantra would be: "As long as I can make money, then its my value system".

At the one extreme is Zero Value System, whereby anything goes, you don't care whether its syndicated ramping or the owner is a bastard, or anything, as long as you can buy and sell at a profit, thats all that matters. Anything beyond that is superfluous to you.

Legality - This should be first level of screening. Most of us would not touch something even if it makes us money if its illegal, e.g. money laundering, Ponzi schemes, etc.

Religion - The most well known is the Shariah compliant investing, self explanatory, no harm industries. We may not see this is Asia but its popular in the US, Christian based funds. Generally, they stay away from porn, tobacco, liquor, gaming and firearms. There are also Catholic Funds, specifically, this means the fund never invests in companies involved in abortion or pornography, nor does it invest in any company that contributes to Planned Parenthood. The fund also screens out companies that offer nonmarital partner benefits. These funds certainly give a new meaning to the "value investing", or rather "values investing".

Green Values - So you may not be so religiously inclined, but you may feel strongly about investing in companies that "behaves properly" in terms of maintaining a sustainable ecosystem, minimal damage to the environment, green corporate philosophies, into renewable energies, promotes resource efficiencies, etc.

Moralistic Fine Lines - Are you OK buying gaming companies, knowing full well that many families would have been wrecked by excessive gaming addiction, and these companies prey on these exact people to maintain their profits? How about if a a company operated brothels professionally, do you want to participate and support a company that reaps profits from "exploitation of the flesh"?

GLCs - Maybe this applies just to Malaysia, but Mr. Koon and I have the same "value system", we stay away from GLCs. This is because the whole structure of GLCs in Malaysia feeds mostly from patronage and contracts awardment. We have not seen a good display of management superiority or the ability to galvanise resources and advantages to move to the next level. So, generally we stay away from investing in GLCs.

Political - Obvious reasons. If you strongly political, you will not want to participate in the companies that benefit from the "ties and advantages" of being in bed with certain political heavyweights.

Syndicate Stocks - Most Malaysians have no qualms about touching syndicated stocks, they say that if they don't trade in them, there'd be nothing left to trade!!?? Then there are those who strongly abhor these stocks, by virtue of participating in them, you are akin to supporting their manipulative behaviour. Most Malaysians think this is a grey area or necessary evil, rather than a sinister behaviour.

Treatment of Minority Interests - This one again eludes most Malaysians investors as an issue of concern. To me, this is a major concern. To cite examples, some may think that the privatisation and relisting of Bumi Armada may have "over-trampled" on minority interests. Some would say the same for Felda Global Ventures. In my case, I won't be buying any of the two until I feel that MI has been properly treated.

So, what is your personal investing values' system?

At the one extreme is Zero Value System, whereby anything goes, you don't care whether its syndicated ramping or the owner is a bastard, or anything, as long as you can buy and sell at a profit, thats all that matters. Anything beyond that is superfluous to you.

Legality - This should be first level of screening. Most of us would not touch something even if it makes us money if its illegal, e.g. money laundering, Ponzi schemes, etc.

Religion - The most well known is the Shariah compliant investing, self explanatory, no harm industries. We may not see this is Asia but its popular in the US, Christian based funds. Generally, they stay away from porn, tobacco, liquor, gaming and firearms. There are also Catholic Funds, specifically, this means the fund never invests in companies involved in abortion or pornography, nor does it invest in any company that contributes to Planned Parenthood. The fund also screens out companies that offer nonmarital partner benefits. These funds certainly give a new meaning to the "value investing", or rather "values investing".

Green Values - So you may not be so religiously inclined, but you may feel strongly about investing in companies that "behaves properly" in terms of maintaining a sustainable ecosystem, minimal damage to the environment, green corporate philosophies, into renewable energies, promotes resource efficiencies, etc.

Moralistic Fine Lines - Are you OK buying gaming companies, knowing full well that many families would have been wrecked by excessive gaming addiction, and these companies prey on these exact people to maintain their profits? How about if a a company operated brothels professionally, do you want to participate and support a company that reaps profits from "exploitation of the flesh"?

GLCs - Maybe this applies just to Malaysia, but Mr. Koon and I have the same "value system", we stay away from GLCs. This is because the whole structure of GLCs in Malaysia feeds mostly from patronage and contracts awardment. We have not seen a good display of management superiority or the ability to galvanise resources and advantages to move to the next level. So, generally we stay away from investing in GLCs.

Political - Obvious reasons. If you strongly political, you will not want to participate in the companies that benefit from the "ties and advantages" of being in bed with certain political heavyweights.

Syndicate Stocks - Most Malaysians have no qualms about touching syndicated stocks, they say that if they don't trade in them, there'd be nothing left to trade!!?? Then there are those who strongly abhor these stocks, by virtue of participating in them, you are akin to supporting their manipulative behaviour. Most Malaysians think this is a grey area or necessary evil, rather than a sinister behaviour.

Treatment of Minority Interests - This one again eludes most Malaysians investors as an issue of concern. To me, this is a major concern. To cite examples, some may think that the privatisation and relisting of Bumi Armada may have "over-trampled" on minority interests. Some would say the same for Felda Global Ventures. In my case, I won't be buying any of the two until I feel that MI has been properly treated.

So, what is your personal investing values' system?

Saturday, June 09, 2012

What If Unemployment Hits 20% In Asia? (Revisited)

As usual, the employers are the ones opposing the much needed unemployment benefits plan by the government. Any additional costs will always be frowned upon by employers. But what are the key issues here:

a) a more cohesive, inclusive society, that tries to lessen overall burden during hard times

b) the lack of safety nets for Malaysian workers in the labour markets, we are left to fend for ourselves the moment we are out of a job, that is not the sign of a developing caring nation

c) cost will rise, but some cost are necessary to achieve higher goals, we cannot keep a low cost structure all the time as that will only keep fostering low yield, sunset industries for the economy

d) although 20% is scary, we will be in pretty tough waters even if it just goes to 6%-7%

e) we have a "too structured civil service", if we employ the scheme, we may be able to do strategic "staff attrition" without as much fallout or displacement in the future

-------------------------------

(Malaysian Insider) KUALA LUMPUR, June 9 — The federal government plans to introduce unemployment benefits by pushing through legislation as early as September, a move that has angered small-medium enterprises (SME) as employers could bear 40 per cent of the cost.

The Malaysian Insider has learnt that Putrajaya completed consultations with stakeholders at local and national levels last month for unemployment insurance (UI), with a proposed contribution from the government and employers each doubling what employees fork out.

Teh wondered whether employers can digest another compulsory cost from the government.

A source said the government is looking at announcing the move as soon as September, the same month Prime Minister Datuk Seri Najib Razak will table Budget 2013, likely before leading Barisan Nasional (BN) into polls for the first time.

“The UI is for those retrenched after confirmation. There has been a proposal that those confirmed after three months of work be compensated for up to 24 months,” the source told The Malaysian Insider.

But SMEs, who have previously complained of crippling wage bills under the minimum wage policy announced on Labour Day, are questioning the need for more compulsory labour costs.

They say they were left in the dark over UI until a few weeks ago. The Small-Medium Industry Association of Malaysia (SMIAM) has since pressured the Human Resources Ministry and the Social Security Organisation (Socso) into a dialogue session to be held today.

SMIAM president Teh Kee Sin told The Malaysian Insider that they were left out of earlier consultations despite being the hardest hit from any hike in labour costs.

SMEs, which make up 99 per cent of operational companies and employ 59 per cent of the labour force, or seven million workers, are the most labour-intensive, with 15 per cent of manufacturing costs coming from human resource.

“We have no idea what the progress is. What we want to know is whether this is to replace compensation already set out in the Employment Act or a new parallel system. We are already making compulsory monthly contributions for Socso and the Human Resources Development Fund.

“The government is now attempting to introduce UI. Can we digest another compulsory cost from the government?” Teh asked, saying that the move “seems to promote unemployment” rather than aid the local export-oriented economy amid global financial troubles. According to the Malaysian Trades Union Congress (MTUC), the umbrella body representing 800,000 workers from 390 unions, the government completed “regional and national satellite workshops on May 24 to gain feedback” from the three main stakeholders, i.e., the government, employers and workers.

Abdul Halim said the government was drafting legislation to introduce the scheme.

“The steering committee is led by Socso. The International Labour Organisation (ILO) has been involved from the start and will send in their expert advice by the end of June,” MTUC secretary-general Abdul Halim Mansor told The Malaysian Insider.

The Malaysian Insider also reported this week that general elections will likely be delayed until November to allow the ruling BN to shore up support with Deputy Prime Minister Tan Sri Muhyiddin Yassin suggesting that more cash handouts are in store.

Putrajaya has previously toyed with the idea of a retrenchment fund to be set up with equal contributions from both employers and employees but the plan was met with scepticism from companies.

The UI appears to be a revival of the idea as Abdul Halim had also told The Malaysian Insider last month that the government was drafting legislation to introduce the fund.

Most developed economies practise a form of unemployment benefit, with the United Kingdom practising a Jobseekers’ Allowance (JSA), commonly known as “the dole.”

The British scheme compels those seeking welfare payments to commit to actively seeking employment but imposes no time limit, leading to accusations that many of the 5.5 million on the dole are purposely trying to remain unemployed.

The United States, however, imposes a 99-week limit on unemployment benefits.

But headwinds from the euro-zone crisis and a cooling Chinese economy has hit Malaysian exports, slowing growth to 4.7 per cent for the first three months of the year, the third consecutive quarterly drop since Q2 2011.

Several manufacturing associations told The Malaysian Insider recently they are already “cautious” and looking to “consolidate rather than expand” over the next 18 months without added pressure on their balance sheets from contributions to UI.

Teh also warned the Najib administration not to go down the same path as the controversial minimum wage policy “where they only consulted us at the last minute” over the move which the SMIAM said would add 30 per cent to employers’ labour costs.

“We want time to give our input, to object and protest if need be,” he said.

Previous Postings

The experience of the current Eurozone crisis, in particular with respect to unemployment, has enormous lessons for Asian economies. Yes, we did navigate our way out of the 97 financial tsunami after a couple of years. The thing is, in most Asian countries there are very few safety nets. Once you lose your jobs, thats it, you are out on your own. You have mortgages, education fees for your kids, extended family financial support payments, car loans, credit card loans, etc ... The dislocation can be enormous.

We can learn from the E.U. experience by implementing our own unemployment insurance scheme (opinion at end of posting). We were relatively lucky in that the 97 Asian crisis was relatively "minor" compared to the current E.U. combustion.

Look at the current unemployment rate in E.U.:

Spain 23.3%

Greece 20.7%

Portugal 14.8%

Give that to any Asian country, you can see massive unrest, maybe even riots. The real unemployment rate is also skewed negatively for younger people, hence you can gauge the resentment.

However, why the situation is still relatively "calm" over in Europe is because of their relatively generous unemployment insurance scheme. You will gawk with envy, but we should all learn something from this before it comes around to our shores. And you can bet that such events will go around the world if history is any guide.

Wednesday, February 11, 2009

Our government has been postponing the need for unemployment insurance for too long. We do not have sufficient safety nets underpinning our country's social and economic systems. The concern has always been the cost side. The other argument is the incentive not to work. There is a bigger danger in having unemployment insurance - companies may be more "willing" to bite the bullet to lay off workers in such an environment.

We already have too many archaic rules pervading the economic life of Malaysians. Its quite debilitating really. We have no unemployment insurance, and every 7-10 years we will have a massive recession and many might not be able to honour their commitments owing to forces greater than them.

We can take the pedestal and say they deserve it for not being able to manage their financial affairs properly, but seriously, even drug addicts and prisoners get a second chance to rebuild their lives. I am not here to justify reckless behaviour, but to ask that the laws be fairer to the normal person. When you unfairly penalises a person, it does not just affect the person alone, in Malaysia's culture, people also have to take care of their parents and extended families. Hence the social impact is substantial.

I am not an insurance guy, but I think we can come up with a semi government body to do this, or even be part of EPF to do this. EPF can do this role well as it already has the database for checks and balances.

How about all employees contribute 1.5% to this Fund and the employer puts in another matching 1.5% of salary. Only employees who have contributed more than 1 year will be able to enjoy the benefits. If you are laid off, you will get 3 months full pay and 5 months of half pay of your last salary.These will be paid like normal salaries on a monthly basis, thus covering most expenses for at least 8 months. This will be in additional to the normal notice pay and severance pay. Once you have taken the unemployment benefits, you will need to be working for at least another year before being qualified to obtain the benefits again.

Like I said I am no actuary, but all things being equal, the monthly 3% to the fund basically means 1 person is covered for every 33 employees. All things being equal again, in a downturn the Fund should be more than able to carry a 300 basis point jump in unemployment (e.g. if unemployment rate jumps from 3.5% to 6.5%, technically speaking we are better equipped to deal with it). EPF has the database and will be able to verify when a person has found new employment. In any system there will be bad hats trying to find loopholes - heavy penalties should be meted out to discourage bad behaviour by employers and employees.

During good times, the Fund will be able to accumulate surpluses, thus covering the outflows during bad times. It is not meant to be a crutch but part of a developing structure for a developing nation, that seeks to minimise social costs, where we can grow and shoulder the good and bad together. Any major shortfall will be borne by the government, which won't be necessary if the calculations are made properly. Its not a crutch really because its NOT borne by the taxpayers but by the contributors to the insurance scheme. That 8 months of pay will be very important as many are shouldering mortgages that needs to be serviced - its not like, no job then can go back to kampung and stay with parents or live off the land. Let's be realistic.

a) a more cohesive, inclusive society, that tries to lessen overall burden during hard times

b) the lack of safety nets for Malaysian workers in the labour markets, we are left to fend for ourselves the moment we are out of a job, that is not the sign of a developing caring nation

c) cost will rise, but some cost are necessary to achieve higher goals, we cannot keep a low cost structure all the time as that will only keep fostering low yield, sunset industries for the economy

d) although 20% is scary, we will be in pretty tough waters even if it just goes to 6%-7%

e) we have a "too structured civil service", if we employ the scheme, we may be able to do strategic "staff attrition" without as much fallout or displacement in the future

-------------------------------

(Malaysian Insider) KUALA LUMPUR, June 9 — The federal government plans to introduce unemployment benefits by pushing through legislation as early as September, a move that has angered small-medium enterprises (SME) as employers could bear 40 per cent of the cost.

The Malaysian Insider has learnt that Putrajaya completed consultations with stakeholders at local and national levels last month for unemployment insurance (UI), with a proposed contribution from the government and employers each doubling what employees fork out.

Teh wondered whether employers can digest another compulsory cost from the government.

A source said the government is looking at announcing the move as soon as September, the same month Prime Minister Datuk Seri Najib Razak will table Budget 2013, likely before leading Barisan Nasional (BN) into polls for the first time.

“The UI is for those retrenched after confirmation. There has been a proposal that those confirmed after three months of work be compensated for up to 24 months,” the source told The Malaysian Insider.

But SMEs, who have previously complained of crippling wage bills under the minimum wage policy announced on Labour Day, are questioning the need for more compulsory labour costs.

They say they were left in the dark over UI until a few weeks ago. The Small-Medium Industry Association of Malaysia (SMIAM) has since pressured the Human Resources Ministry and the Social Security Organisation (Socso) into a dialogue session to be held today.

SMIAM president Teh Kee Sin told The Malaysian Insider that they were left out of earlier consultations despite being the hardest hit from any hike in labour costs.

SMEs, which make up 99 per cent of operational companies and employ 59 per cent of the labour force, or seven million workers, are the most labour-intensive, with 15 per cent of manufacturing costs coming from human resource.

“We have no idea what the progress is. What we want to know is whether this is to replace compensation already set out in the Employment Act or a new parallel system. We are already making compulsory monthly contributions for Socso and the Human Resources Development Fund.

“The government is now attempting to introduce UI. Can we digest another compulsory cost from the government?” Teh asked, saying that the move “seems to promote unemployment” rather than aid the local export-oriented economy amid global financial troubles. According to the Malaysian Trades Union Congress (MTUC), the umbrella body representing 800,000 workers from 390 unions, the government completed “regional and national satellite workshops on May 24 to gain feedback” from the three main stakeholders, i.e., the government, employers and workers.

Abdul Halim said the government was drafting legislation to introduce the scheme.

“The steering committee is led by Socso. The International Labour Organisation (ILO) has been involved from the start and will send in their expert advice by the end of June,” MTUC secretary-general Abdul Halim Mansor told The Malaysian Insider.

The Malaysian Insider also reported this week that general elections will likely be delayed until November to allow the ruling BN to shore up support with Deputy Prime Minister Tan Sri Muhyiddin Yassin suggesting that more cash handouts are in store.

Putrajaya has previously toyed with the idea of a retrenchment fund to be set up with equal contributions from both employers and employees but the plan was met with scepticism from companies.

The UI appears to be a revival of the idea as Abdul Halim had also told The Malaysian Insider last month that the government was drafting legislation to introduce the fund.

Most developed economies practise a form of unemployment benefit, with the United Kingdom practising a Jobseekers’ Allowance (JSA), commonly known as “the dole.”

The British scheme compels those seeking welfare payments to commit to actively seeking employment but imposes no time limit, leading to accusations that many of the 5.5 million on the dole are purposely trying to remain unemployed.

The United States, however, imposes a 99-week limit on unemployment benefits.

But headwinds from the euro-zone crisis and a cooling Chinese economy has hit Malaysian exports, slowing growth to 4.7 per cent for the first three months of the year, the third consecutive quarterly drop since Q2 2011.

Several manufacturing associations told The Malaysian Insider recently they are already “cautious” and looking to “consolidate rather than expand” over the next 18 months without added pressure on their balance sheets from contributions to UI.

Teh also warned the Najib administration not to go down the same path as the controversial minimum wage policy “where they only consulted us at the last minute” over the move which the SMIAM said would add 30 per cent to employers’ labour costs.

“We want time to give our input, to object and protest if need be,” he said.

Previous Postings

The experience of the current Eurozone crisis, in particular with respect to unemployment, has enormous lessons for Asian economies. Yes, we did navigate our way out of the 97 financial tsunami after a couple of years. The thing is, in most Asian countries there are very few safety nets. Once you lose your jobs, thats it, you are out on your own. You have mortgages, education fees for your kids, extended family financial support payments, car loans, credit card loans, etc ... The dislocation can be enormous.

We can learn from the E.U. experience by implementing our own unemployment insurance scheme (opinion at end of posting). We were relatively lucky in that the 97 Asian crisis was relatively "minor" compared to the current E.U. combustion.

Look at the current unemployment rate in E.U.:

Spain 23.3%

Greece 20.7%

Portugal 14.8%

Give that to any Asian country, you can see massive unrest, maybe even riots. The real unemployment rate is also skewed negatively for younger people, hence you can gauge the resentment.

However, why the situation is still relatively "calm" over in Europe is because of their relatively generous unemployment insurance scheme. You will gawk with envy, but we should all learn something from this before it comes around to our shores. And you can bet that such events will go around the world if history is any guide.

Germany: in accordance with the social code, financed by obligatory social contributions of all workers, the unemployment insurance is allocated for a period depending on the age and on the duration of contributions to the unemployed who can justify at least 12 working months in the last 3 years. The unemployment assistance, financed by tax, complements the unemployment benefits for people who have exhausted their rights. The benefit rates are 60% of the net salary for unemployed without children and 67% for unemployed with children. Specific measures are set for older unemployed Austria: a system very close to the German system is defined by the law. Benefit rates are 55% of the net salary for the unemployment insurance and 92% of the minimum income for the unemployment assistance.

Belgium: Defined by the law, unemployment benefits are financed by an obligatory contribution of workers. They are allocated for an unlimited duration under the condition to have been working for 312 days in the last 18 months or 624 days in the last 36 months. Their level is defined by a percentage of the previous average salary limited to 63 € a day, 60% the first year and 44% the following years for a single person, 60% for people with dependant family members, 55% the first year for « coinhabitants » (unmarried couple living under the same roof) without dependent family members. Specific measures are set for older unemployed.

Denmark: defined by the law, the principle is based on the voluntary contribution of the worker. Benefits are allocated on the condition to have been working 52 weeks during the last 3 years and to have been affiliated to a fund for at least one year. The entitlement duration is one year (6 months for young under 25’s), then at the most 3 years on the condition to participate in different measures against unemployment. The benefit rate is 90% of the reference salary and limited to 1624 € a month (1232 for young under 25). Specific measures are set for older unemployed.

Spain: The unemployment insurance is defined by the law. It is financed by obligatory social contributions. It is allocated to unemployed who have worked at least 360 days in the last 6 years for a period from 4 months to 2 years according to the paid contributions. The amount is worth 70% of the reference salary for the first 182 days and then 60%. Specific measures are set for older unemployed. The unemployment assistance complements the unemployment benefits during 6 to 18 months at the most for people who have exhausted their rights. The unemployment assistance is worth 75% of the minimum wage during the first 6 months.

Finland: Defined by the law, the system is made of an unemployment insurance divided in two parts: a basic allowance for those who have worked 43 weeks during the last 24 months with a minimum of 18 hours a week and an allowance proportional to incomes for those who affiliated to a voluntary fund during the same period. The entitlement duration is 500 days. The basic allowance is a bit less than 23 € and the proportional allowance adds 42% of the difference between the daily wage and the basic allowance. Young people aged 17 who have not finished their training course or the ones aged from 18 to 25 who refused employment schemes or training are excluded from the system. Specific measures are set for older unemployed. The unemployment assistance covers those who are not entitled or have exhausted their rights. The amount is equal to the basic allowance.

France: The unemployment insurance is defined by long term agreements between employer's organizations and trade unions that administrate the UNEDIC which is a private law organization. These agreements must respect the principles of the labour law and thus be officially approved by the government. The financing is ensured by contributions based on the salaries paid by employers and workers. The duration of entitlement vary from 7 to 42 months in accordance with the previous working period and the age. The amount is worth 57,4% of the gross salary of reference. A specific solidarity allowance (ASS) takes over the unemployed insurance for the unemployed who have exhausted their rights, under some conditions, specifically the level of the family income. At the most, the ASS is worth 13,57 € a day (19,47 for older unemployed aged more than 55). Until now, the entitlement was unlimited, but the question was raised to limit it to 2 years, Nethertheless, this measure is under discussion. There are some complicated systems for older unemployed.

Greece: Defined by the law, the unemployment insurance is allocated to unemployed workers who have a sickness insurance affiliation to a social security organization, and who have worked at least 125 days during the last 14 months or 200 days during the last 2 years before their redundancy. The duration of the entitlement depends on the duration of the previous working period. The amount of allowances is worth 50% of the daily wage or 50% of the monthly salary depending on the worker's status. Specific measures are set for older unemployed.

Ireland: The unemployed insurance system is defined by the law. It is financed by obligatory contributions taken out of the salaries. Allowances are allocated to unemployed who have paid contributions during 39 weeks in the year before their redundancy or 26 weeks during the two previous years for an entitlement of a maximum of 390 days. The allowances are uniform and are worth 475 €. Specific measures are set for older unemployed. The unemployment assistance, financed by tax takes over the allowances for those who have exhausted their rights, it is depending on resources conditions and is worth 475 €.

Italy: defined by the law, the system covers full unemployment and short time unemployment. Allowances are given to unemployed who have paid at least 52 monthly contributions in a 2 years period. People are entitled for a maximum of 180 days (270 for unemployed older than 50). The amount is 40% of the salary of reference for the 3 last month preceding the redundancy with a limit of 760 € for salaries below 1644 € and 913 for the others. As for short time unemployment, a supplement is added on the salary to workers in firms of specific category and locality which do not fit with demanded conditions enabling to be under the full employment system. There is not any specific measure are set for older unemployed.

Luxembourg: Defined by the law, the system ensures an unemployed allowance to those who have worked at least 26 weeks during the year before the redundancy. The standard duration of entitlement is one year and can be extended to 182 days for unemployed who have difficulties to find a job, it can also be extended to durations depending on the duration of affiliation for people older than 50. The allowance rate is worth 80% of the salary of reference. Specific measures are set for older unemployed.

Netherlands: The system is defined by the law. Allowances are allocated to unemployed who have worked at least 26 weeks in the last 39 weeks. The duration varies between 9 months and 4 years. The allowance rate is worth 70% of the last salary with a maximum daily amount of 159 €. Specific measures are set for older unemployed.

Portugal: Defined by the law, the system is based on a social insurance regime compulsory for workers. It is completed by the unemployment assistance for those who are not entitled to unemployment insurance. Allowances are allocated to those who have worked at least 540 days during the last 24 months before their redundancy, for a period going from 12 to 30 months at the most and according to the age. The amount is worth 65% of the salary of reference. The unemployment assistance is allocated to those who can justify 180 working days during the last 12 months. The entitlement periods follow the same rules as the unemployment insurance but when assistance allowances are allocated after people have been allocated insurance allowances, the duration is divided by two. The amount of the unemployment assistance allowances are worth 80% of the minimum wage. Older unemployed are compulsorily retired when their rights are exhausted.

United Kingdom: defined by the law, the system provides an unemployment allowance financed by compulsory social contributions of workers and an assistance financed by tax. Allowances are allocated according to family resources conditions for a period of a maximum of 182 days as far as insurance is concerned and an unlimited period for the assistance. The basic rates of these allowances are 340 € a month (204 for young aged 16 – 17, 268 for the 18-24) and 523 € for a couple. There is not any specific measure are set for older unemployed.

Sweden: Defined by the law, the system has two constituents: an allowance proportional to the income (80% of the income) for people who chose to affiliate an unemployment insurance fund for at least 12 months; a basic allowance for people older than 20 For an East – West solidarity of the social movements years old who cannot get the proportional allowance and who have worked at least 6 months, 70 hours a month. The basic allowance is allocated for 300 days at the most and is worth 29 € a day. There is not any specific measure set for older unemployed.

----------------------------------

Our government has been postponing the need for unemployment insurance for too long. We do not have sufficient safety nets underpinning our country's social and economic systems. The concern has always been the cost side. The other argument is the incentive not to work. There is a bigger danger in having unemployment insurance - companies may be more "willing" to bite the bullet to lay off workers in such an environment.

We already have too many archaic rules pervading the economic life of Malaysians. Its quite debilitating really. We have no unemployment insurance, and every 7-10 years we will have a massive recession and many might not be able to honour their commitments owing to forces greater than them.

We can take the pedestal and say they deserve it for not being able to manage their financial affairs properly, but seriously, even drug addicts and prisoners get a second chance to rebuild their lives. I am not here to justify reckless behaviour, but to ask that the laws be fairer to the normal person. When you unfairly penalises a person, it does not just affect the person alone, in Malaysia's culture, people also have to take care of their parents and extended families. Hence the social impact is substantial.

I am not an insurance guy, but I think we can come up with a semi government body to do this, or even be part of EPF to do this. EPF can do this role well as it already has the database for checks and balances.

How about all employees contribute 1.5% to this Fund and the employer puts in another matching 1.5% of salary. Only employees who have contributed more than 1 year will be able to enjoy the benefits. If you are laid off, you will get 3 months full pay and 5 months of half pay of your last salary.These will be paid like normal salaries on a monthly basis, thus covering most expenses for at least 8 months. This will be in additional to the normal notice pay and severance pay. Once you have taken the unemployment benefits, you will need to be working for at least another year before being qualified to obtain the benefits again.

Like I said I am no actuary, but all things being equal, the monthly 3% to the fund basically means 1 person is covered for every 33 employees. All things being equal again, in a downturn the Fund should be more than able to carry a 300 basis point jump in unemployment (e.g. if unemployment rate jumps from 3.5% to 6.5%, technically speaking we are better equipped to deal with it). EPF has the database and will be able to verify when a person has found new employment. In any system there will be bad hats trying to find loopholes - heavy penalties should be meted out to discourage bad behaviour by employers and employees.

During good times, the Fund will be able to accumulate surpluses, thus covering the outflows during bad times. It is not meant to be a crutch but part of a developing structure for a developing nation, that seeks to minimise social costs, where we can grow and shoulder the good and bad together. Any major shortfall will be borne by the government, which won't be necessary if the calculations are made properly. Its not a crutch really because its NOT borne by the taxpayers but by the contributors to the insurance scheme. That 8 months of pay will be very important as many are shouldering mortgages that needs to be serviced - its not like, no job then can go back to kampung and stay with parents or live off the land. Let's be realistic.

Friday, June 08, 2012

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

Tuesday, June 05, 2012

Shanghai Index Shaming China's Government?

This is uncanny. Can this be tweaked? Now there should be a big crackdown to look for "culprits".

China's share benchmark has fallen foul of the country's internet censors by appearing to mark the 23rd anniversary of the Tiananmen Square crackdown on pro-democracy protesters.

In an unlikely coincidence certainly unwelcome to China's communist rulers, the stock benchmark fell 64.89 points on Monday, matching the numbers of the June 4, 1989 crackdown in the heart of Beijing.

In China's lively microblog world, 'Shanghai Composite Index' soon joined the many words blocked by internet censors.

Coincidence ... China's share benchmark fell 64.89 points on Monday, matching the numbers of the June 4, 1989 Tiananmen Square crackdown.

In another odd twist, the index opened Monday at 2,346.98. That is being interpreted as 23rd anniversary of the June 4, 1989 crackdown when read from right to left.

Public discussion of the Tiananmen crackdown, which the Communist Party branded a "counter-revolutionary riot", remains taboo. Analysts refused to comment on the numbers.

On the popular Sina microblog site, searches using 'June 4', '64.89', 'stock market', and 'benchmark Shanghai Composite Index' were all blocked.

Such searches draw the response: "According to law such words cannot be shown."

In Beijing, the anniversary passed without any major sign of protest. The front page of the party newspaper, People's Daily, trumpeted the "Stable, fast development of the Chinese economy: Advancing to be the World's No.2".

The melee as soldiers fought their way into Beijing to clear Tiananmen Square is believed to have left hundreds dead. In response to the violence in the capital, demonstrations erupted in more than 180 cities.

Foreign Ministry spokesman Liu Weimin objected to a US State Department call for a reconsideration of the party's stance as "rude interference in China's internal affairs".

In the semi-autonomous Chinese city of Hong Kong, tens of thousands crowded into a large park to mark the anniversary. They held aloft white candles that transformed the area of soccer pitches into a sea of light, before observing a minute of silence.

Read more: http://www.smh.com.au/business/world-business/china-stock-index-evokes-tiananmen-with-6489point-fall-20120605-1zsoe.html#ixzz1wsgdYT8w

China's share benchmark has fallen foul of the country's internet censors by appearing to mark the 23rd anniversary of the Tiananmen Square crackdown on pro-democracy protesters.

In an unlikely coincidence certainly unwelcome to China's communist rulers, the stock benchmark fell 64.89 points on Monday, matching the numbers of the June 4, 1989 crackdown in the heart of Beijing.

In China's lively microblog world, 'Shanghai Composite Index' soon joined the many words blocked by internet censors.

Coincidence ... China's share benchmark fell 64.89 points on Monday, matching the numbers of the June 4, 1989 Tiananmen Square crackdown.

In another odd twist, the index opened Monday at 2,346.98. That is being interpreted as 23rd anniversary of the June 4, 1989 crackdown when read from right to left.

Public discussion of the Tiananmen crackdown, which the Communist Party branded a "counter-revolutionary riot", remains taboo. Analysts refused to comment on the numbers.

On the popular Sina microblog site, searches using 'June 4', '64.89', 'stock market', and 'benchmark Shanghai Composite Index' were all blocked.

Such searches draw the response: "According to law such words cannot be shown."

In Beijing, the anniversary passed without any major sign of protest. The front page of the party newspaper, People's Daily, trumpeted the "Stable, fast development of the Chinese economy: Advancing to be the World's No.2".

The melee as soldiers fought their way into Beijing to clear Tiananmen Square is believed to have left hundreds dead. In response to the violence in the capital, demonstrations erupted in more than 180 cities.

Foreign Ministry spokesman Liu Weimin objected to a US State Department call for a reconsideration of the party's stance as "rude interference in China's internal affairs".

In the semi-autonomous Chinese city of Hong Kong, tens of thousands crowded into a large park to mark the anniversary. They held aloft white candles that transformed the area of soccer pitches into a sea of light, before observing a minute of silence.

Read more: http://www.smh.com.au/business/world-business/china-stock-index-evokes-tiananmen-with-6489point-fall-20120605-1zsoe.html#ixzz1wsgdYT8w

Monday, June 04, 2012

Commodities Correction - Something Sinister In The Works?

We can all appreciate stock markets correcting with the E.U. crisis somehow managing to find more things to worry about. However, the smarter ones would have been asking why the commodities have been falling way before stocks, and now seems only going stronger in its downfall together with global equities.

Commodities have been a good gauge of the strength of economic recovery. Hence are we saying the global economy is headed for a tailspin? A minor correction is understandable but the way they have been correcting implies there is something graver in the works.

Price of oil has fallen into a hole, so much so that it is below some of the OPEC members' production cost even. Other commodities have done likewise. What was interesting was that although gold did perk up, it did not reflect a stampede to get out of all assets with the fear of inflation in mind.

The negative yield into German papers indicate that people are rushing to solid currencies. Before we venture further let's look at the 2011 asset class returns. Almost everything went into a hole except for bonds, corn and oil. Hence we cannot say there had been any over exuberance over the past 18 months.

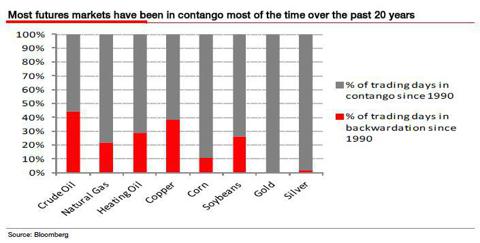

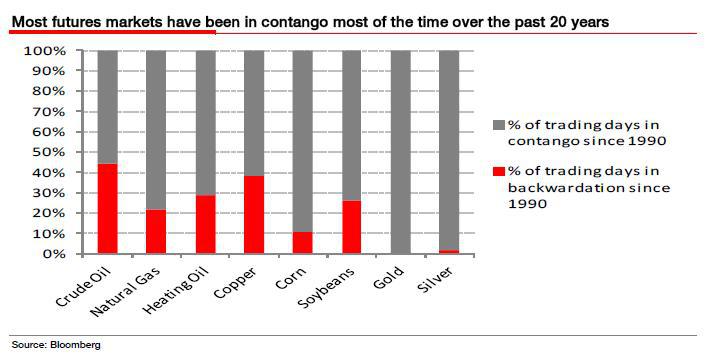

The Contango Effect

Malaysian market players from the 90s would be well aware of the word contango. Say you buy shares with minimal deposit or no deposit for say RM100,000 and you have no bloody intention of picking them up, or have the ability to. You have to rollover, that's contango. In the futures markets for commodities, a substantial portion of trades are contango trades.

Final Word - I do not think this is developing into a catastrophic scenario. I believe the correction in commodities is more a congruence of factors aligning itself at the same time. Nothing much to do but sit and wait.

Commodities have been a good gauge of the strength of economic recovery. Hence are we saying the global economy is headed for a tailspin? A minor correction is understandable but the way they have been correcting implies there is something graver in the works.

Price of oil has fallen into a hole, so much so that it is below some of the OPEC members' production cost even. Other commodities have done likewise. What was interesting was that although gold did perk up, it did not reflect a stampede to get out of all assets with the fear of inflation in mind.

The negative yield into German papers indicate that people are rushing to solid currencies. Before we venture further let's look at the 2011 asset class returns. Almost everything went into a hole except for bonds, corn and oil. Hence we cannot say there had been any over exuberance over the past 18 months.

| 2011 Sector Performance | Performance | Potentially Similar ETF |

| Utilities | 13.10% | (XLU) |

| Healthcare | 10% | (XLV) |

| Services | 4.20% | n/a |

| Consumer Goods | 2.60% | (XLP) |

| Technology | -3.60% | (XLK) |

| Conglomerates | -3.90% | n/a |

| Indusrial Goods | -4.90% | (XLI) |

| Basic Materials | -10.40% | (XLB) |

| Financials | -18.80% | (XLF) |

| 2011 Capitalization Performance | Performance | Potentially Similar ETF |

| Large | -4.40% | (SPY) |

| Mid | -4.60% | (MDY) |

| Mega | -6.60% | (DIA) |

| Nano | -8.30% | n/a |

| Small | -9.10% | (IJR) |

| Micro | -16.10% | (IWC) |

| 2011 Index Price Performance | Performance | Potentially Similar ETF |

| S&P 500 | -0.02% | |

| Shanghai | -22.42% | (FXI) |

| Nikkei 225 | -17.34% | (EWJ) |

| Hang Seng Index | -19.27% | (EWH) |

| Euro Stoxx 50 | -18.41% | (FEU) |

| S&P/TSX Composite Index | -11.01% | (EWC) |

| 2011 Currency Performance | Performance | Potentially Similar ETF |

| EUR/USD | -1.30% | n/a |

| USD/JPY | -5.91% | n/a |

| USD/CAD | 1.64% | n/a |

| USD/CNY | -4.62% | n/a |

Note: currency ETFs do exist, but without detailed explanation of how they work I thought it prudent to leave out the tickers.

| 2011 Commodity Performance | Performance | Potentially Similar ETF |

| Gold | 10.19% | (GLD) |

| Oil | 6.33% | (DBO) |

| Natural Gas | -42.21% | (GAZ) |

| Silver | -9.75% | (SLV) |

| Copper | -19.56% | (JJC) |

| Wheat | -23.89% | (JJA) |

| Soybeans | -5.81% | " |

| Corn | 15.43% | " |

| 2011 Bond ETF Performance | Performance | ETF Used in Calculation |

| Long Term US Treasuries | 30.25% | (TLT) |

| iShares Aggregate Bond Fund | 4.68% | (AGG) |

| TIPS | 9.28% | (TIP) |

| Investment Grade | 5.17% | (LQD) |

| High Yield | -0.78% | (HYG) |

The Contango Effect

Malaysian market players from the 90s would be well aware of the word contango. Say you buy shares with minimal deposit or no deposit for say RM100,000 and you have no bloody intention of picking them up, or have the ability to. You have to rollover, that's contango. In the futures markets for commodities, a substantial portion of trades are contango trades.

A simple explanation for the commodities price fall would be that investors and traders have given up rolling over positions and just squaring. Generally in contango trades, you are usually long. It is infrequent that contango trades being short trades. Many hedge funds or large investors do contango trades because of the "super cycle theory", which Jim Rogers is famed for, i.e. we are supposedly on a very long bull run for commodities.

There are probably contributing factors to the diminishing contango positions: more ideal weather patterns for agriculture products (a weakened La Nina), a genuine reassessment that the China engine may not be as strong as first thought. Lump that in with the renewed E.U. crisis implosion (European elections), you have a potent mix.

Final Word - I do not think this is developing into a catastrophic scenario. I believe the correction in commodities is more a congruence of factors aligning itself at the same time. Nothing much to do but sit and wait.

Subscribe to:

Posts (Atom)